Last month, Reserve Bank of India (RBI) released the report of the Expert Committee on Urban Co-operative Banks (Chair: Mr. N. S. Vishwanathan). In this blog, we discuss some broader issues with the functioning and regulation of urban co-operative banks (UCBs), and some of the suggestions to address these as highlighted by the committee in its report.

Need for Urban Co-operative Banks

The history of UCBs in India can be traced to the 19th century when such societies were set up drawing inspiration from the success of the co-operative movement in Britain and the co-operative credit movement in Germany. Urban co-operative credit societies, were organised on a community basis to meet the consumption-oriented credit needs of their members. UCBs are primary cooperative banks in urban and semi-urban areas. They are co-operative societies that undertake banking business. Co-operative banks accept deposits from the public and lend to their members. Co-operative banks are different from other co-operatives as they mobilise resources for lending and investment from the wider public rather than only their members.

Concerns regarding the professionalism of urban cooperative banks gave rise to the view that they should be better regulated. Large cooperative banks with paid-up share capital and reserves of one lakh rupees were brought under the scope of the Banking Regulation Act, 1949 with effect from March 1, 1966. Prior to this, such banks were regulated under the scope of state-specific cooperative laws. The revised framework brought them under the ambit of supervision of the RBI. Till 1996, these banks could lend money only for non-agricultural purposes. However, this distinction does not apply today.

The Expert Committee noted that UCBs play a key role in financial inclusion. It further observed that the focus area for UCBs has traditionally been communities and localities including workplace groups. They play an important role in the delivery of last-mile credit, even more so for those sections of the population who are not integrated into the mainstream banking framework. UCBs primarily lend to wage earners, small entrepreneurs, and businesses in urban and semi-urban areas. UCBs can be more responsive than formal banking channels to the needs of the local people.

Over the years, concerns have been raised about non-professional management in UCBs and that this can lead to weaker governance and risk management in these entities. RBI has also taken regulatory action on several UCBs. For instance, in September 2019, RBI placed Punjab and Maharashtra Co-operative Bank under restrictions on allegations of serious underreporting of non-performing assets. The bank could not grant loans, make investments or accept deposits without prior approval from RBI. While these restrictions were originally put in place for six months, the time frame was extended several times and has now been extended till December 31, 2021. In addition, low capital base, poor credit management and diversion of funds have also been issues in the sector.

Shrinking share in the banking sector

There were 1,539 UCBs in the country as of March 31, 2020, with deposits worth Rs 5,01,180 crore and advances worth Rs 3,05,370 crore. Even though 94% of the entities in the banking sector were UCBs their market share in the banking sector has been low and declining and stands at around 3%. UCBs accounted for 3.24% of the deposits and 2.69% of the advances in the banking sector. The Committee noted that state-of-the-art technology adopted by new players, such as small finance banks and fintech entities, along with commercial banks can disrupt the niche customer segment of the UCBs.

|

Figure 1: Growth in deposits of UCBs (in Rs crore) |

Figure 2: Growth in advances of UCBs (in Rs crore) |

Burden of non-performing assets

UCBs had the highest net non-performing asset (NNPA) ratio (5.26%) and gross non-performing asset (GNPA) ratio (10.96%) across the banking sector as of March 2020. These levels correspond to around twice that of private sector banks, and around five times that of small finance banks. The Committee noted that, as of March 2020, UCBs have the lowest level of net interest margin (difference between interest earned and interest spent relative to total interest generating assets held by the bank) and negative return on assets and return on equity.

Figure 3: Asset quality across banks (in percentage)

Sources: Report of the Expert Committee on Urban Co-operative Banks; PRS.

Supervisory Action Framework (SAF): SAF envisages corrective action by UCB and/or supervisory action by RBI on breach of financial thresholds related to asset quality, profitability and level of capital as measured by Capital to Risk-weighted Asset Ratio (CRAR). The Committee recommended that SAF should consider only asset quality (based on net non-performing asset ratio) and CRAR with an emphasis on reducing the time spent by a UCB under SAF. The RBI should begin the mandatory resolution process including reconstruction or compulsory merger as soon as a UCB reaches the third stage under SAF (CRAR less than 4.5% and/or net non-performing asset ratio above 12%).

Constraints in raising capital

The Committee also observed that UCBs are constrained in raising capital which restricts their ability to expand the business. According to co-operative principles, share capital is to be issued and refunded only at face value. Thus, investment in UCBs is less attractive as it does not lead to an increase in its value. Also, the principle of one member, one vote means that an interested investor cannot acquire a controlling stake in UCBs. It was earlier recommended that UCBs should be allowed to issue fresh capital at a premium based on the net worth of the entity at the end of the preceding year.

Listing of securities: The Committee recommended making suitable amendments to the Banking Regulation Act, 1949 to enable RBI to notify certain securities issued by any co-operative bank or class of co-operative banks to be covered under the Securities Contracts (Regulation) Act, 1956 and the Securities and Exchange Board of India Act, 1992. This will enable their listing and trading on a recognised stock exchange. Until such amendments are made, the Committee recommended that banks can be allowed to have a system on their websites to buy/sell securities at book value subject to the condition that the bank should ensure that the prospective buyer is eligible to be admitted as a member.

Conflict between Banking Regulation Act, 1949 and co-operative laws

The fundamental difference between banking companies and co-operative banks is in the voting rights of shareholders. In banking companies, each share has a corresponding vote. But in the case of co-operative banks, each shareholder has only one vote irrespective of the number of shares held. Despite RBI being the regulator of the banking sector, the regulation of co-operative banks by RBI was restricted to functions related directly to banking. This gave rise to dual regulation with governance, audit, and winding-up related functions regulated by state governments and central government for single-state banks and multi-state banks, respectively.

2020 Amendments to the Banking Regulation Act: In September 2020, the Banking Regulation Act, 1949 was amended to increase RBI’s powers over the regulation of co-operative banks including qualifications of management of these banks and supersession of board of directors. The Committee noted that due to the amendment of the Act, certain conflicts have arisen with various co-operative laws. For instance, the Act allows co-operative banks to issue shares at a premium, but it is silent on their redemption. It noted that if any co-operative societies’ legislation provides for redemption of shares only at par, then, while a co-operative bank incorporated under that legislation can issue shares at a premium, it can redeem them only at par.

Note that on September 3, 2021, the Madhya Pradesh High Court stayed a circular released by the RBI on appointment of managing director/whole-time director in UCBs. The circular provided for eligibility and propriety criteria for the appointment of such personnel in UCBs. The petitioner, Mahanagar Nagrik Sahakari Bank Maryadit, argued that the service conditions of the managing director and chief executive officer of co-operative banks are governed by bye-laws framed under the M.P. State Cooperative Societies Act, 1960. The petition noted that co-operative as a subject falls under the state list and hence the power to legislate in the field of co-operative societies falls under the domain of the states and not the central government.

Umbrella Organisation

Over the years, several committees have looked at the feasibility to set up an Umbrella Organisation (UO) for UCBs. It is an apex body of federating UCBs. In 2011, an expert committee on licensing of new UCBs recommended that there should be two separate UOs for the sector. In June 2019, RBI granted an in-principle approval to National Federation of Urban Co-operative Banks and Credit Societies Ltd to set up a UO in the form of a non-deposit taking non-banking finance company. The UO is expected to provide information technology and financial support to its federating members along with value-added services linked to treasury, foreign exchange and international remittances. It is envisaged to provide scale through network to smaller UCBs. The report of the current Committee recommended that the minimum capital of the UO should be Rs 300 crore. Once stabilised, the UO can explore the possibility of becoming a universal bank. It can also take up the role of a self-regulatory organisation for its member UCBs. The Committee also suggested that the membership of the UO can be opened-up to both financial and non-financial co-operatives who can make contributions through share capital in the UO.

Comments on the report of the Expert Committee are invited until September 30, 2021.

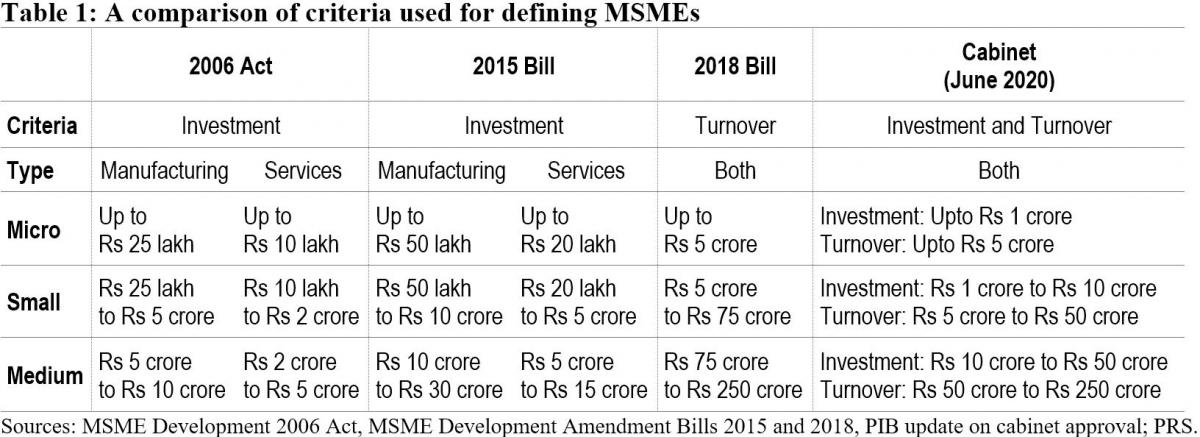

On June 1, 2020, the Cabinet Committee on Economic Affairs approved a revision in the definition of Micro, Small and Medium Enterprises (MSMEs).[1] In this blog, we discuss the change in the definition as approved by the Cabinet, and examine some of the common criteria used for classification of MSMEs.

Currently, MSMEs are defined under the Micro, Small and Medium Enterprises Development Act, 2006.[2] The Act classifies them as micro, small and medium enterprises based on: (i) investment in plant and machinery for enterprises engaged in manufacturing or production of goods, and (ii) investment in equipment for enterprises providing services. As per the Cabinet approval, the investment limits will be revised upwards and annual turnover of the enterprise will be used as additional criteria for the classification of MSMEs (Table 1).

Earlier attempts to amend the definition of MSMEs

The central government has sought to revise the definition of MSMEs in the Act on two earlier occasions. The government introduced the MSME Development (Amendment) Bill, 2015 which proposed to increase the investment limits for manufacturing and services MSMEs.[3] This Bill was withdrawn in July 2018 and another Bill was introduced. The MSME Development (Amendment) Bill, 2018 proposed to: (i) use annual turnover as criteria instead of investment for classification of MSMEs, (ii) remove the distinction between manufacturing and services, and (iii) provide the central government with the power to revise the turnover limits, through a notification.[4] The 2018 Bill lapsed with the dissolution of 16th Lok Sabha.

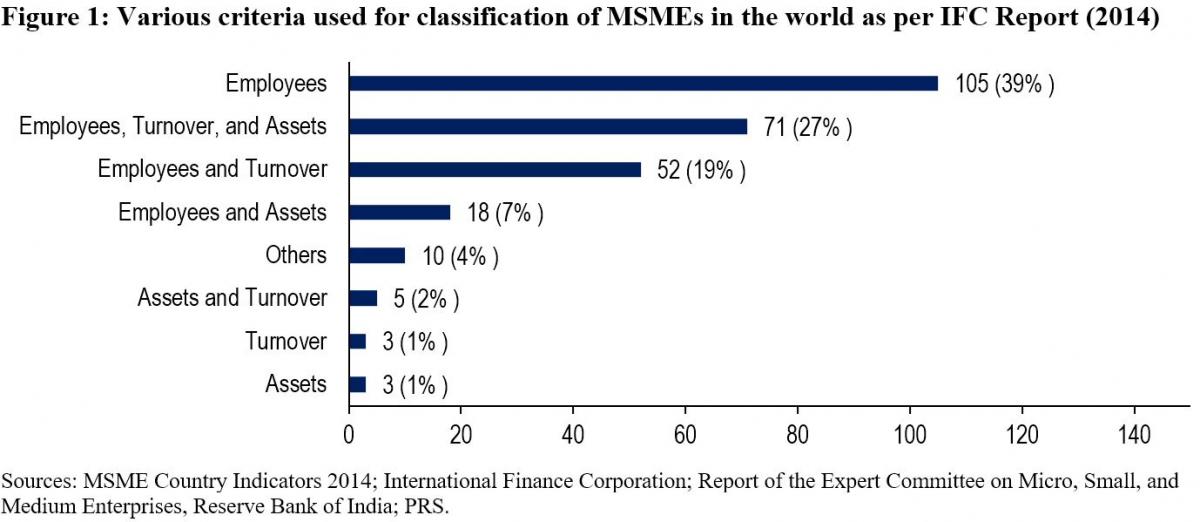

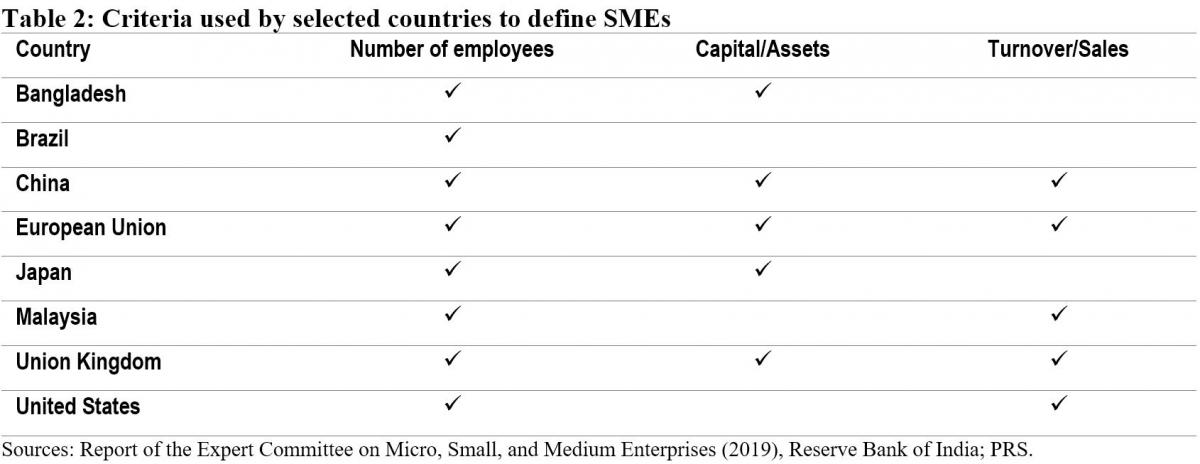

Global trends in criteria for the classification of MSMEs

While India will now be using investment and annual turnover as the criteria to classify MSMEs, globally, the number of employees is the most widely used criteria for classifying MSMEs. The Reserve Bank of India's Expert Committee on MSMEs (2019) cited a study by the International Finance Corporation in 2014 which analysed 267 definitions used by different institutions in 155 countries.[5],[6] According to the study, countries used a combination of criteria to classify MSMEs. 92% of the definitions used the number of employees as one of the criteria. Other frequently used criteria were: (i) turnover (49%), and (ii) value of assets (36%). 11% of the analysed definitions used alternative criteria such as: (i) loan size, (ii) years of experience, and (iii) initial investment.

Evaluation of common criteria used to define MSMEs

Investment: The 2006 Act uses investment in plant, machinery, and equipment to classify MSMEs. Some of the issues with the investment criteria include:

Due to their informal and small scale of operations, firms often do not maintain proper books of accounts and hence find it difficult to get classified as MSMEs as per the current definition.5

The investment-based classification incentivises promoters to keep the investment size restricted to retain the benefits associated with the micro or small category.7

Turnover: The 2018 Bill sought to replace the investment criteria with annual turnover as the sole criteria for the classification of MSMEs. The Standing Committee agreed with the proposal under the Bill to use annual turnover as the criteria instead of investment.7 It observed that this could overcome some of the shortcomings of classification based on investment. While turnover based criteria will also require verification, the Committee noted that the GST Network (GSTN) data can act as a reliable source of information for this purpose. However, it also observed that:7

With turnover as a criterion for classification, corporates may misuse the incentives meant for MSMEs. For instance, there is a possibility that a multi-national company may produce a large quantity of products worth a high turnover and then market it through various subsidiaries registered as Micro or Small enterprise under GSTN.

The turnover of some enterprises may fluctuate depending on their business, which may result in the change of classification of the enterprise during a year.

The Committee noted that there is a wide gap in turnover limits. For instance, an enterprise with a turnover of Rs 6 crore and an enterprise with a turnover of Rs 75 crore (as proposed in 2018 Bill) would both be classified as a small enterprise, which seems incongruous.

The Expert Committee (RBI) also recommended using annual turnover as the criteria for classification instead of investment.5 It observed that turnover based definition would be transparent, progressive, and easier to implement through the GSTN. It also recommended that the power to change the definition of MSMEs should be delegated to the executive as it will help in responding to changing economic scenarios.

Number of employees: The Standing Committee had highlighted that in a labour-intensive country like India, appropriate focus is required on employment generation and MSME sector is the most suitable platform for this.7 It had recommended that the central government should assess the number of persons employed in the MSME sector and also consider employment as a criterion while classifying MSMEs. However, the Expert Committee (RBI) stated that while the employment-based definition is an additional feature preferred in some countries, the definition would pose challenges in implementation.5 According to the Ministry of MSME, employment as a criterion has problems due to: (i) factors such as seasonality and informal nature of engagement, (ii) similar to investment criteria, this would also require physical verification and has associated cost overheads.7

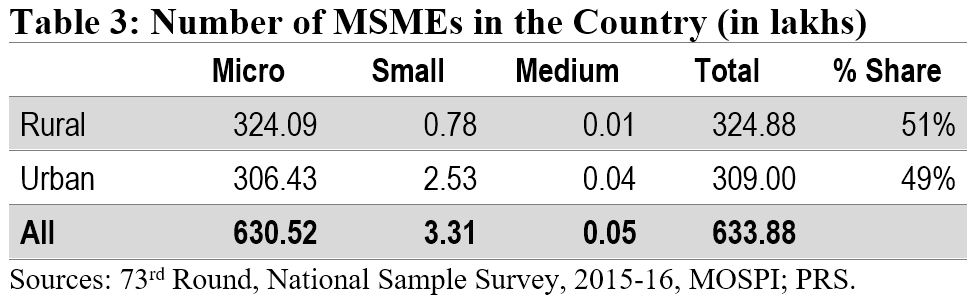

Number of MSMEs

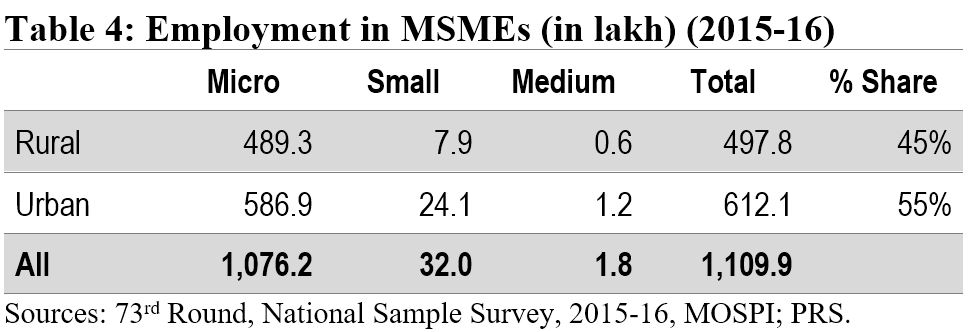

According to the National Sample Survey (2015-16), there were around 6.34 crore MSMEs in the country. The micro sector with 6.3 crore enterprises accounted for more than 99% of the total estimated number of MSMEs. The small and medium sectors accounted for only 0.52% and 0.01% of the estimated number of enterprises, respectively. Another dataset to understand the distribution of MSMEs is Udyog Aadhaar, a unique identity provided by the Unique Identification Authority of India (UIDAI) to MSME enterprises.[8] Udyog Aadhaar registration is based on self-declaration by enterprises. Between September 2015 and June 2020, 98.6 lakh enterprises have registered with UIDAI. According to this dataset, micro, small, and medium enterprises comprise 87.7%, 11.8% and 0.5% of the MSME sector respectively.

Employment in the MSME sector

The MSME sector employed nearly 11.1 crore people in 2015-16. The sector was the second largest employer after the agriculture sector. The highest number of employed persons were engaged in trade activity (35%), followed by persons engaged in manufacturing (32%).

Implications of change in the definition of MSMEs

The change in the definition of MSMEs may result in many enterprises which are currently classified as Small enterprises be reclassified as Micro, and those classified as Medium enterprises be reclassified as Small. Further, there may be many enterprises which are not currently classified as MSMEs, which may fall under the MSME classification as per the new definition. Such enterprises will also now benefit from the schemes related to MSMEs. The Ministry of MSME runs various schemes to provide for: (i) flow of credit to MSMEs, (ii) support for technology upgrade and modernisation, (iii) entrepreneurship and skill development, and (iv) cluster-wise measures to promote capacity-building and empowerment of MSME units. For instance, under the Credit Guarantee Fund Scheme for Micro and Small Enterprises, a credit guarantee cover of up to 75% of the credit is provided to micro and small enterprises.[9] Thus, the re-classification may require a significant increase in budgetary allocation for the MSME sector.

Other announcements related to MSMEs in the aftermath of COVID-19

MSME sector accounted for nearly 33.4% of the total manufacturing output in 2017-18.[10] During the same year, its share in the country’s total exports was around 49%. Between 2015 and 2017, the contribution of the sector in GDP has been around 30%. Due to the national lockdown induced by COVID-19, businesses including MSMEs have been badly hit. To provide immediate relief to the MSME sector, the government announced several measures in May 2020.[11] These include: (i) collateral-free loans for MSMEs with up to Rs 25 crore outstanding and up to Rs 100 crore turnover, (ii) Rs 20,000 crore as subordinate debt for stressed MSMEs, and (iii) Rs 50,000 crore of capital infusion into MSMEs. These measures have also been approved by the Union Cabinet.[12]

For more details on the announcements made under the Aatma Nirbhar Bharat Abhiyan, see here.

[1] “Cabinet approves Upward revision of MSME definition and modalities/ road map for implementing remaining two Packages for MSMEs (a)Rs 20000 crore package for Distressed MSMEs and (b) Rs 50,000 crore equity infusion through Fund of Funds”, Press Information Bureau, Cabinet Committee on Economic Affairs, June 1, 2020.

[2] The Micro, Small and Medium Enterprises Development Act, 2006, https://samadhaan.msme.gov.in/WriteReadData/DocumentFile/MSMED2006act.pdf.

[3] The Micro, Small and Medium Enterprises Development (Amendment) Bill, 2015, https://www.prsindia.org/sites/default/files/bill_files/MSME_bill%2C_2015_0.pdf.

[4] The Micro, Small and Medium Enterprises Development (Amendment) Bill, 2018, https://www.prsindia.org/sites/default/files/bill_files/The%20Micro%2C%20Small%20and%20Medium%20Enterprises%20Development%20%28Amendment%29%20Bill%2C%202018%20Bill%20Text.pdf.

[5] Report of the Expert Committee on Micro, Small and Medium Enterprises, The Reserve Bank of India, July 2019, https://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/MSMES24062019465CF8CB30594AC29A7A010E8A2A034C.PDF.

[6] MSME Country Indicators 2014, International Finance Corporation, December 2014, https://www.smefinanceforum.org/sites/default/files/analysis%20note.pdf.

[7] 294th Report on Micro Small and Medium Enterprises Development (Amendment) Bill 2018, Standing Committee on Industry, Rajya Sabha, December 2018, https://rajyasabha.nic.in/rsnew/Committee_site/Committee_File/ReportFile/17/111/294_2019_3_15.pdf.

[8] Enterprises with Udyog Aadhaar Number, National Portal for Registration of Micro, Small & Medium Enterprises, Ministry of Micro, Small and Medium Enterprises, https://udyogaadhaar.gov.in/UA/Reports/StateBasedReport_R3.aspx.

[9] Credit Guarantee Fund Scheme for Micro and Small Enterprises, Ministry of Micro, Small and Medium Enterprises, http://www.dcmsme.gov.in/schemes/sccrguarn.htm.

[10] Annual Report 2018-19, Ministry of Micro, Small and Medium Enterprises, https://msme.gov.in/sites/default/files/Annualrprt.pdf.

[11] "Finance Minister announce measures for relief and credit support related to businesses, especially MSMEs to support Indian Economy’s fight against COVID-19", Press Information Bureau, Ministry of Finance, May 13, 2020.

[12] "Cabinet approves additional funding of up to Rupees three lakh crore through introduction of Emergency Credit Line Guarantee Scheme (ECLGS)", Press Information Bureau, Ministry of Finance, May 20, 2020.