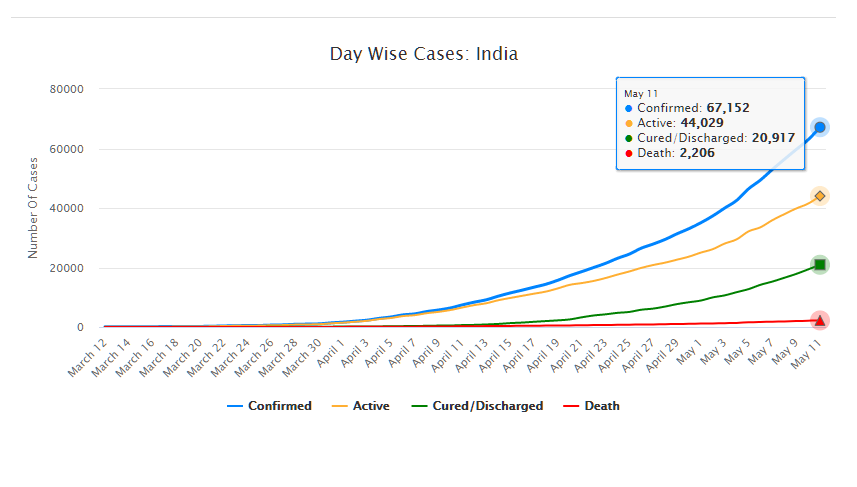

As of May 11, 2020, there are 67,152 confirmed cases of COVID-19 in India. Since May 4, 24,619 new cases have been registered. Out of the confirmed cases so far, 20,917 patients have been cured/discharged and 2,206 have died. As the spread of COVID-19 has increased across the country, the central government has continued to announce several policy decisions to contain the spread, and support citizens and businesses who are being affected by the pandemic. In this blog post, we summarise some of the key measures taken by the central government in this regard between May 4 and May 11, 2020.

Source: Ministry of Health and Family Welfare; PRS.

Industry

Relaxation of labour laws in some states

The Gujarat, Himachal Pradesh, Rajasthan, Haryana, and Uttarakhand governments have passed notifications to increase maximum weekly work hours from 48 hours to 72 hours and daily work hours from 9 hours to 12 hours for certain factories. This was done to combat the shortage of labour caused by the lockdown. Further, some state governments stated that longer shifts would ensure a fewer number of workers in factories so as to allow for social distancing.

Madhya Pradesh has promulgated the Madhya Pradesh Labour Laws (Amendment) Ordinance, 2020. The Ordinance exempts establishments with less than 100 workers from adhering to the Madhya Pradesh Industrial Employment (Standing Orders) Act, 1961, which regulates the conditions of employment of workers. Further, it allows the state government to exempt any establishment or class of establishments from the Madhya Pradesh Shram Kalyan Nidhi Adhiniyam, 1982, which provides for the constitution of a welfare fund for labour.

The Uttar Pradesh government has published a draft Ordinance which exempts all factories and establishments engaged in manufacturing processes from all labour laws for a period of three years. Certain conditions will continue to apply with regard to payment of wages, safety, compensation and work hours, amongst others. However, labour laws providing for social security, industrial dispute resolution, trade unions, strikes, amongst others, will not apply under the Ordinance.

Financial aid

Central government signs an agreement with Asian Infrastructure Investment Bank for COVID-19 support

The central government and Asian Infrastructure Investment Bank (AIIB) signed a 500 million dollar agreement for the COVID-19 Emergency Response and Health Systems Preparedness Project. The project aims to help India respond to the COVID-19 pandemic and strengthen India’s public health system to manage future disease outbreaks. The project is being financed by the World Bank and AIIB in the amount of 1.5 billion dollars, of which one billion dollars is being provided by World Bank and 500 million dollars is being provided by AIIB. This financial support will be available to all states and union territories and will be used to address the needs of at-risk populations, medical personnel, and creating medical and testing facilities, amongst others. The project will be implemented by the National Health Mission, the National Center for Disease Control, and the Indian Council of Medical Research, under the Ministry of Health and Family Welfare.

Travel

Restarting of passenger travel by railways

Indian Railways plans to restart passenger trains from May 12 onwards. It will begin with 15 pairs of trains which will run from New Delhi station connecting Dibrugarh, Agartala, Howrah, Patna, Bilaspur, Ranchi, Bhubaneswar, Secunderabad, Bengaluru, Chennai, Thiruvananthapuram, Madgaon, Mumbai Central, Ahmedabad and Jammu Tawi. Booking for reservation in these trains will start at 4 pm on May 11. Thereafter, Indian Railways plans to start more services on new routes.

Return of Indians stranded abroad

The central government will facilitate the return of Indian nationals stranded abroad in a phased manner beginning on May 7. The travel will be arranged by aircraft and naval ships. The stranded Indians utilising the service will be required to pay for it. Medical screening of the passengers will be done before the flight. On reaching India, passengers will be required to download the Aarogya Setu app. Further, they will be quarantined by the concerned state government in either a hospital or a quarantine institution for 14 days on a payment basis. After quarantine, passengers will be tested for COVID-19 and further action will be taken based on the results.

For more information on the spread of COVID-19 and the central and state government response to the pandemic, please see here.

The Enforcement of Security Interest and Recovery of Debts Laws and Miscellaneous Provisions (Amendment) Bill, 2016 is listed for discussion in Rajya Sabha today.[i] The Bill aims to expeditiously resolve cases of debt recovery by making amendments to four laws, including the (i) Recovery of Debts Due to Banks and Financial Institutions Act, 1993, and (ii) the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002. Recovery of Debts Due to Banks and Financial Institutions Act, 1993 The 1993 Act created Debt Recovery Tribunals (DRTS) to adjudicated debt recovery cases. This was done to move cases out of civil courts, with the idea of reducing time taken for debt recovery, and for providing technical expertise. This was aimed at assisting banks and financial institutions in recovering outstanding debt from defaulters. Over the years, it has been observed that the DRTs do not comply with the stipulated time frame of resolving disputes within six months. This has resulted in delays in disposal, and a high pendency of cases before the DRTs. Between March 2013 and December 2015, the number of pending cases before the DRTs increased from 43,000 to 70,000. With an average disposal rate of 10,000 cases per year, it is estimated that these DRTs will take about six to seven years to clear the existing backlog of cases.[ii] Experts have also observed that the DRT officers, responsible for debt recovery, lack experience in dealing with such cases. Further, these officers are not adequately trained to adjudicate debt-related matters.[iii] The 2016 Bill proposes to increase the retirement age of Presiding Officers of DRTs, and allows for their reappointment. This will allow the existing DRT officers to serve for longer periods of time. However, such a move may have limited impact in expanding the pool of officers in the DRTs. The 2016 Bill also has a provision which allows Presiding Officers of tribunals, established under other laws, to head DRTs. Currently, there are various specialised tribunals functioning in the country, like the Securities Appellate Tribunal, the National Company Law Tribunal, and theNational Green Tribunal. It remains to be seen if the skills brought in by officers of these tribunals will mirror the specialisation required for adjudicating debt-related matters. Further, the 1993 Act provides that banks and financial institutions must file cases in those DRTs that have jurisdiction over the defendant’s area of residence or business. In addition, the Bill allows cases to be filed in DRTs having jurisdiction over the bank branch where the debt is due. The Bill also provides that certain procedures, such as presentation of claims by parties and issue of summons by DRTs, can now be undertaken in electronic form (such as filing them on the DRT website). Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 The 2002 Act allows secured creditors (lenders whose loans are backed by a security) to take possession over a collateral security if the debtor defaults in repayment. This allows creditors to sell the collateral security and recover the outstanding debt without the intervention of a court or a tribunal. This takeover of collateral security is done with the assistance of the District Magistrate (DM), having jurisdiction over the security. Experts have noted that the absence of a time-limit for the DM to dispose such applications has resulted in delays.[iv] The 2016 Bill proposes to introduce a 30-day time limit within which the DM must pass an order for the takeover of a security. Under certain circumstances, this time-limit may be extended to 60 days. The 2002 Act also regulates the establishment and functioning of Asset Reconstruction Companies (ARCs). ARCs purchase Non-Performing Assets (NPAs) from banks at a discount. This allows banks to recover partial payment for an outstanding loan account, thereby helping them maintain cash flow and liquidity. The functioning of ARCs has been explained in Figure 1.  It has been observed that the setting up of ARCs, along with the use out-of-court systems to take possession of the collateral security, has created an environment conducive to lending.[iii] However, a few concerns related to the functioning of ARCs have been expressed over the years. These concerns include a limited number of buyers and capital entering the ARC business, and high transaction costs involved in the transfer of assets in favour of these companies due to the levy of stamp duty.[iii] In this regard, the Bill proposes to exempt the payment of stamp duty on transfer of financial assets in favour of ARCs. This benefit will not be applicable if the asset has been transferred for purposes other than securitisation or reconstruction (such as for the ARCs own use or investment). Consequently, the Bill amends the Indian Stamp Act, 1899. The Bill also provides greater powers to the Reserve Bank of India to regulate ARCs. This includes the power to carry out audits and inspections either on its own, or through specialised agencies. With the passage of the Bankruptcy Code in May 2016, a complete overhaul of the debt recovery proceedings was envisaged. The Code allows creditors to collectively take action against a defaulting debtor, and complete this process within a period of 180 days. During the process, the creditors may choose to revive a company by changing the repayment schedule of outstanding loans, or decide to sell it off for recovering their dues. While the Bankruptcy Code provides for collective action of creditors, the proposed amendments to the SARFAESI and DRT Acts seek to streamline the processes of creditors individually taking action against the defaulting debtor. The impact of these changes on debt recovery scenario in the country, and the issue of rising NPAs will only become clear in due course of time. [i] Enforcement of Security Interest and Recovery of Debts Laws and Miscellaneous Provisions (Amendment) Bill, 2016, http://www.prsindia.org/administrator/uploads/media/Enforcement%20of%20Security/Enforcement%20of%20Security%20Bill,%202016.pdf. [ii] Unstarred Question No. 1570, Lok Sabha, Ministry of Finance, Answered on March 4, 2016. [iii] ‘A Hundred Small Steps’, Report of the Committee on Financial Sector Reforms, Planning Commission, September 2008, http://planningcommission.nic.in/reports/genrep/rep_fr/cfsr_all.pdf. [iv] Financial Sector Legislative Reforms Commission, March 2013, http://finmin.nic.in/fslrc/fslrc_report_vol1.pdf.

It has been observed that the setting up of ARCs, along with the use out-of-court systems to take possession of the collateral security, has created an environment conducive to lending.[iii] However, a few concerns related to the functioning of ARCs have been expressed over the years. These concerns include a limited number of buyers and capital entering the ARC business, and high transaction costs involved in the transfer of assets in favour of these companies due to the levy of stamp duty.[iii] In this regard, the Bill proposes to exempt the payment of stamp duty on transfer of financial assets in favour of ARCs. This benefit will not be applicable if the asset has been transferred for purposes other than securitisation or reconstruction (such as for the ARCs own use or investment). Consequently, the Bill amends the Indian Stamp Act, 1899. The Bill also provides greater powers to the Reserve Bank of India to regulate ARCs. This includes the power to carry out audits and inspections either on its own, or through specialised agencies. With the passage of the Bankruptcy Code in May 2016, a complete overhaul of the debt recovery proceedings was envisaged. The Code allows creditors to collectively take action against a defaulting debtor, and complete this process within a period of 180 days. During the process, the creditors may choose to revive a company by changing the repayment schedule of outstanding loans, or decide to sell it off for recovering their dues. While the Bankruptcy Code provides for collective action of creditors, the proposed amendments to the SARFAESI and DRT Acts seek to streamline the processes of creditors individually taking action against the defaulting debtor. The impact of these changes on debt recovery scenario in the country, and the issue of rising NPAs will only become clear in due course of time. [i] Enforcement of Security Interest and Recovery of Debts Laws and Miscellaneous Provisions (Amendment) Bill, 2016, http://www.prsindia.org/administrator/uploads/media/Enforcement%20of%20Security/Enforcement%20of%20Security%20Bill,%202016.pdf. [ii] Unstarred Question No. 1570, Lok Sabha, Ministry of Finance, Answered on March 4, 2016. [iii] ‘A Hundred Small Steps’, Report of the Committee on Financial Sector Reforms, Planning Commission, September 2008, http://planningcommission.nic.in/reports/genrep/rep_fr/cfsr_all.pdf. [iv] Financial Sector Legislative Reforms Commission, March 2013, http://finmin.nic.in/fslrc/fslrc_report_vol1.pdf.