On June 1, 2020, the Cabinet Committee on Economic Affairs approved a revision in the definition of Micro, Small and Medium Enterprises (MSMEs).[1] In this blog, we discuss the change in the definition as approved by the Cabinet, and examine some of the common criteria used for classification of MSMEs.

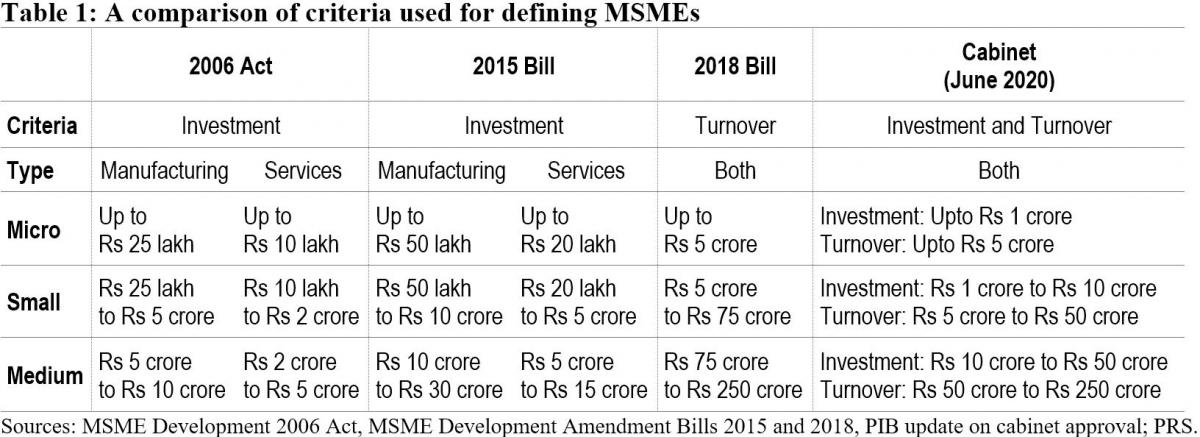

Currently, MSMEs are defined under the Micro, Small and Medium Enterprises Development Act, 2006.[2] The Act classifies them as micro, small and medium enterprises based on: (i) investment in plant and machinery for enterprises engaged in manufacturing or production of goods, and (ii) investment in equipment for enterprises providing services. As per the Cabinet approval, the investment limits will be revised upwards and annual turnover of the enterprise will be used as additional criteria for the classification of MSMEs (Table 1).

Earlier attempts to amend the definition of MSMEs

The central government has sought to revise the definition of MSMEs in the Act on two earlier occasions. The government introduced the MSME Development (Amendment) Bill, 2015 which proposed to increase the investment limits for manufacturing and services MSMEs.[3] This Bill was withdrawn in July 2018 and another Bill was introduced. The MSME Development (Amendment) Bill, 2018 proposed to: (i) use annual turnover as criteria instead of investment for classification of MSMEs, (ii) remove the distinction between manufacturing and services, and (iii) provide the central government with the power to revise the turnover limits, through a notification.[4] The 2018 Bill lapsed with the dissolution of 16th Lok Sabha.

Global trends in criteria for the classification of MSMEs

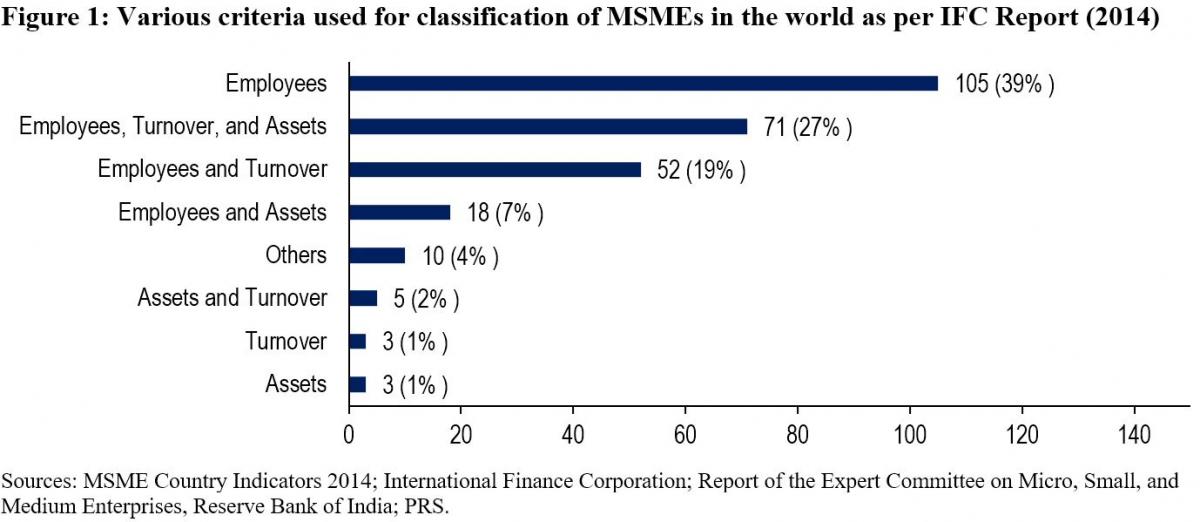

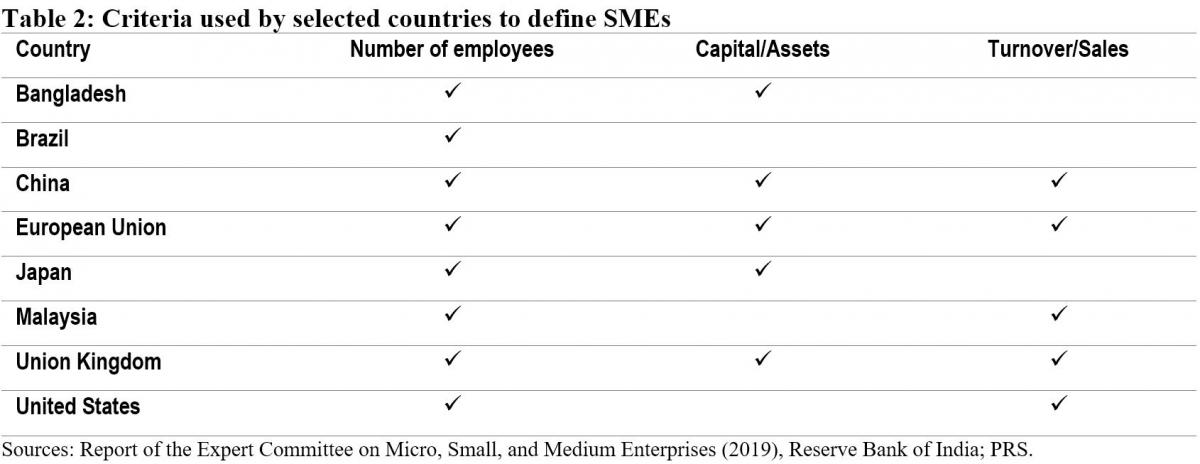

While India will now be using investment and annual turnover as the criteria to classify MSMEs, globally, the number of employees is the most widely used criteria for classifying MSMEs. The Reserve Bank of India's Expert Committee on MSMEs (2019) cited a study by the International Finance Corporation in 2014 which analysed 267 definitions used by different institutions in 155 countries.[5],[6] According to the study, countries used a combination of criteria to classify MSMEs. 92% of the definitions used the number of employees as one of the criteria. Other frequently used criteria were: (i) turnover (49%), and (ii) value of assets (36%). 11% of the analysed definitions used alternative criteria such as: (i) loan size, (ii) years of experience, and (iii) initial investment.

Evaluation of common criteria used to define MSMEs

Investment: The 2006 Act uses investment in plant, machinery, and equipment to classify MSMEs. Some of the issues with the investment criteria include:

Due to their informal and small scale of operations, firms often do not maintain proper books of accounts and hence find it difficult to get classified as MSMEs as per the current definition.5

The investment-based classification incentivises promoters to keep the investment size restricted to retain the benefits associated with the micro or small category.7

Turnover: The 2018 Bill sought to replace the investment criteria with annual turnover as the sole criteria for the classification of MSMEs. The Standing Committee agreed with the proposal under the Bill to use annual turnover as the criteria instead of investment.7 It observed that this could overcome some of the shortcomings of classification based on investment. While turnover based criteria will also require verification, the Committee noted that the GST Network (GSTN) data can act as a reliable source of information for this purpose. However, it also observed that:7

With turnover as a criterion for classification, corporates may misuse the incentives meant for MSMEs. For instance, there is a possibility that a multi-national company may produce a large quantity of products worth a high turnover and then market it through various subsidiaries registered as Micro or Small enterprise under GSTN.

The turnover of some enterprises may fluctuate depending on their business, which may result in the change of classification of the enterprise during a year.

The Committee noted that there is a wide gap in turnover limits. For instance, an enterprise with a turnover of Rs 6 crore and an enterprise with a turnover of Rs 75 crore (as proposed in 2018 Bill) would both be classified as a small enterprise, which seems incongruous.

The Expert Committee (RBI) also recommended using annual turnover as the criteria for classification instead of investment.5 It observed that turnover based definition would be transparent, progressive, and easier to implement through the GSTN. It also recommended that the power to change the definition of MSMEs should be delegated to the executive as it will help in responding to changing economic scenarios.

Number of employees: The Standing Committee had highlighted that in a labour-intensive country like India, appropriate focus is required on employment generation and MSME sector is the most suitable platform for this.7 It had recommended that the central government should assess the number of persons employed in the MSME sector and also consider employment as a criterion while classifying MSMEs. However, the Expert Committee (RBI) stated that while the employment-based definition is an additional feature preferred in some countries, the definition would pose challenges in implementation.5 According to the Ministry of MSME, employment as a criterion has problems due to: (i) factors such as seasonality and informal nature of engagement, (ii) similar to investment criteria, this would also require physical verification and has associated cost overheads.7

Number of MSMEs

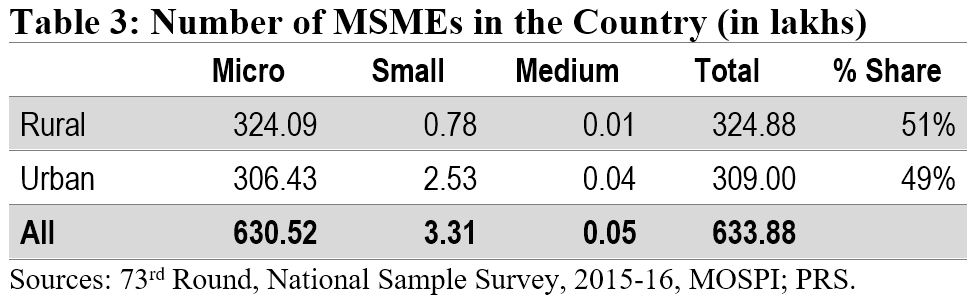

According to the National Sample Survey (2015-16), there were around 6.34 crore MSMEs in the country. The micro sector with 6.3 crore enterprises accounted for more than 99% of the total estimated number of MSMEs. The small and medium sectors accounted for only 0.52% and 0.01% of the estimated number of enterprises, respectively. Another dataset to understand the distribution of MSMEs is Udyog Aadhaar, a unique identity provided by the Unique Identification Authority of India (UIDAI) to MSME enterprises.[8] Udyog Aadhaar registration is based on self-declaration by enterprises. Between September 2015 and June 2020, 98.6 lakh enterprises have registered with UIDAI. According to this dataset, micro, small, and medium enterprises comprise 87.7%, 11.8% and 0.5% of the MSME sector respectively.

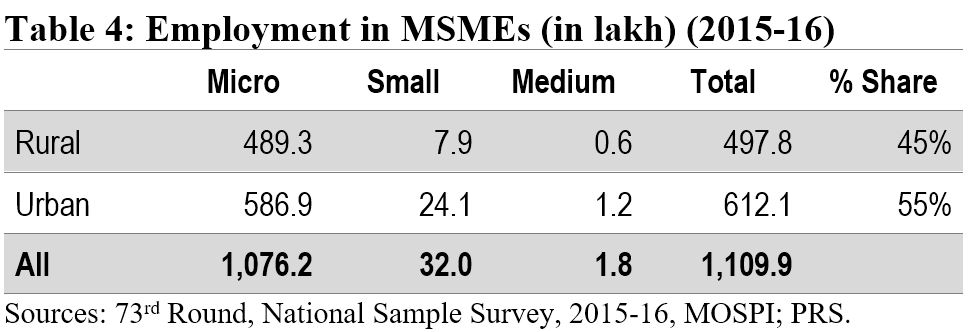

Employment in the MSME sector

The MSME sector employed nearly 11.1 crore people in 2015-16. The sector was the second largest employer after the agriculture sector. The highest number of employed persons were engaged in trade activity (35%), followed by persons engaged in manufacturing (32%).

Implications of change in the definition of MSMEs

The change in the definition of MSMEs may result in many enterprises which are currently classified as Small enterprises be reclassified as Micro, and those classified as Medium enterprises be reclassified as Small. Further, there may be many enterprises which are not currently classified as MSMEs, which may fall under the MSME classification as per the new definition. Such enterprises will also now benefit from the schemes related to MSMEs. The Ministry of MSME runs various schemes to provide for: (i) flow of credit to MSMEs, (ii) support for technology upgrade and modernisation, (iii) entrepreneurship and skill development, and (iv) cluster-wise measures to promote capacity-building and empowerment of MSME units. For instance, under the Credit Guarantee Fund Scheme for Micro and Small Enterprises, a credit guarantee cover of up to 75% of the credit is provided to micro and small enterprises.[9] Thus, the re-classification may require a significant increase in budgetary allocation for the MSME sector.

Other announcements related to MSMEs in the aftermath of COVID-19

MSME sector accounted for nearly 33.4% of the total manufacturing output in 2017-18.[10] During the same year, its share in the country’s total exports was around 49%. Between 2015 and 2017, the contribution of the sector in GDP has been around 30%. Due to the national lockdown induced by COVID-19, businesses including MSMEs have been badly hit. To provide immediate relief to the MSME sector, the government announced several measures in May 2020.[11] These include: (i) collateral-free loans for MSMEs with up to Rs 25 crore outstanding and up to Rs 100 crore turnover, (ii) Rs 20,000 crore as subordinate debt for stressed MSMEs, and (iii) Rs 50,000 crore of capital infusion into MSMEs. These measures have also been approved by the Union Cabinet.[12]

For more details on the announcements made under the Aatma Nirbhar Bharat Abhiyan, see here.

[1] “Cabinet approves Upward revision of MSME definition and modalities/ road map for implementing remaining two Packages for MSMEs (a)Rs 20000 crore package for Distressed MSMEs and (b) Rs 50,000 crore equity infusion through Fund of Funds”, Press Information Bureau, Cabinet Committee on Economic Affairs, June 1, 2020.

[2] The Micro, Small and Medium Enterprises Development Act, 2006, https://samadhaan.msme.gov.in/WriteReadData/DocumentFile/MSMED2006act.pdf.

[3] The Micro, Small and Medium Enterprises Development (Amendment) Bill, 2015, https://www.prsindia.org/sites/default/files/bill_files/MSME_bill%2C_2015_0.pdf.

[4] The Micro, Small and Medium Enterprises Development (Amendment) Bill, 2018, https://www.prsindia.org/sites/default/files/bill_files/The%20Micro%2C%20Small%20and%20Medium%20Enterprises%20Development%20%28Amendment%29%20Bill%2C%202018%20Bill%20Text.pdf.

[5] Report of the Expert Committee on Micro, Small and Medium Enterprises, The Reserve Bank of India, July 2019, https://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/MSMES24062019465CF8CB30594AC29A7A010E8A2A034C.PDF.

[6] MSME Country Indicators 2014, International Finance Corporation, December 2014, https://www.smefinanceforum.org/sites/default/files/analysis%20note.pdf.

[7] 294th Report on Micro Small and Medium Enterprises Development (Amendment) Bill 2018, Standing Committee on Industry, Rajya Sabha, December 2018, https://rajyasabha.nic.in/rsnew/Committee_site/Committee_File/ReportFile/17/111/294_2019_3_15.pdf.

[8] Enterprises with Udyog Aadhaar Number, National Portal for Registration of Micro, Small & Medium Enterprises, Ministry of Micro, Small and Medium Enterprises, https://udyogaadhaar.gov.in/UA/Reports/StateBasedReport_R3.aspx.

[9] Credit Guarantee Fund Scheme for Micro and Small Enterprises, Ministry of Micro, Small and Medium Enterprises, http://www.dcmsme.gov.in/schemes/sccrguarn.htm.

[10] Annual Report 2018-19, Ministry of Micro, Small and Medium Enterprises, https://msme.gov.in/sites/default/files/Annualrprt.pdf.

[11] "Finance Minister announce measures for relief and credit support related to businesses, especially MSMEs to support Indian Economy’s fight against COVID-19", Press Information Bureau, Ministry of Finance, May 13, 2020.

[12] "Cabinet approves additional funding of up to Rupees three lakh crore through introduction of Emergency Credit Line Guarantee Scheme (ECLGS)", Press Information Bureau, Ministry of Finance, May 20, 2020.

India is one of the fastest growing aviation markets in the world. Its domestic traffic makes up 69% of the total airline traffic in South Asia. India’s airport capacity is expected to handle 1 billion trips annually by 2023. The Ministry of Civil Aviation is responsible for formulating national aviation policies and programmes. Today, Lok Sabha will discuss and vote upon the budget of the Ministry of Civil Aviation. In light of this, we discuss key issues with the aviation sector in India.

The aviation sector came under severe financial stress during the Covid-19 pandemic. After air travel was suspended in March 2020, airline operators in India reported losses worth more than Rs 19,500 crore while airports reported losses worth more than Rs 5,120 crore. However, several airline companies were under financial stress before the pandemic affected passenger travel. For instance, in the past 15 years, seventeen airlines have exited the market. Out of those, two airlines, Air Odisha Aviation Pvt Ltd and Deccan Charters Pvt Ltd exited the market in 2020. Air India has been reporting consistent losses over the past four years. All other major private airlines in India such as Indigo and Spice Jet faced losses in 2018-19.

Figure 1: Operating profit/loss of major airlines in India (in Rs crore)

Note: Vistara Airlines commenced operations in 2015, while Air Asia began in 2014; Negative values indicate operating loss.

Source: Unstarred Question 1812 answered on August 4, 2021, and Unstarred Question 1127 answered on September 21, 2020; Rajya Sabha; PRS.

Sale of Air India

Air India has accounted for the biggest expenditure head of the Ministry of Civil Aviation since 2011-12. Between 2009-10 and 2020-21, the government spent Rs 1,22,542 crore on Air India through budgeted allocations. In October 2021, the sale of Air India to Talace Ltd., which is a subsidiary of Tata Sons Pvt Ltd, was approved. The bid for Air India was finalised at Rs 18,000 crore.

Up to January 2020, Air India had accumulated debt worth Rs 60,000 crore. The central government is repaying this debt in the financial year 2021-22. After the finalisation of the sale, the government allocated roughly Rs 71,000 crore for expenses related to Air India.

In addition to loan repayment, in 2021-22, the government will provide Air India with a fresh loan (Rs 4,500 crore) and grants (Rs 1,944 crore) to recover from the shock of Covid-19. To pay for the medical benefits of retired employees of Air India, a recurring expense of Rs 165 crore will be borne by the central government each year.

In 2022-23, Rs 9,260 crore is allocated towards servicing the debt of AIAHL (see Table 1). AIAHL is a Special Purpose Vehicle (SPV) formed by the government to hold the assets and liabilities of Air India while the process of its sale takes place.

Table 1: Breakdown of expenditure on Air India (in Rs crore)

|

Major Head |

2020-21 Actual |

2021-22 RE |

2022-23 BE |

% change from 2021-22 RE to 2022-23 BE |

|

|

Equity infusion in AIAHL |

- |

62,057 |

- |

-100% |

|

|

Debt servicing of AIAHL |

2,184 |

2,217 |

9,260 |

318% |

|

|

Medical benefit to retired employees |

- |

165 |

165 |

0% |

|

|

Loans to AI |

- |

4,500 |

- |

-100% |

|

|

Grants for cash losses during Covid-19 |

- |

1,944 |

- |

-100% |

|

|

Total |

2,184 |

70,883 |

9,425 |

-87% |

|

Note: BE – Budget Estimate; RE – Revised Estimate; AAI: Airports Authority of India; AIAHL – Air India Asset Holding Limited; AI – Air India. Percentage change is from RE 2021-22 to BE 2022-23.

Source: Demands for Grants 2022-23, Ministry of Civil Aviation; PRS.

Privatisation of Airports

Airports Authority of India (AAI) is responsible for creating, upgrading, maintaining and managing civil aviation infrastructure in the country. As on June 23, 2020, it operates and manages 137 airports in the country. Domestic air traffic has more than doubled from around 61 million passengers in 2013-14 to around 137 million in 2019-20. International passenger traffic has grown from 47 million in 2013-14 to around 67 million in 2019-20, registering a growth of over 6% per annum. As a result, airports in India are witnessing rising levels of congestion. Most major airports are operating at 85% to 120% of their handling capacity. In response to this, the government has decided to privatise some airports to address the problem of congestion.

AAI has leased out eight of its airports through Public Private Partnership (PPP) for operation, management and development on long term lease basis. Six of these airports namely, Ahmedabad, Jaipur, Lucknow, Guwahati, Thiruvananthapuram, and Mangaluru have been leased out to M/s Adani Enterprises Limited (AEL) for 50 years (under PPP). The ownership of these airports remains with AAI and the operations will be back with AAI after the concession period is over. The Standing Committee on Transport (2021) had noted that the government expects to have 24 PPP airports by 2024.

Figure 2: Allocation towards AAI (in Rs crore)

Note: BE – Budget Estimate; RE – Revised Estimate; AAI – Airports Authority of India; IEBR – Internal and Extra-Budgetary Resources;

Source: Demand for Grant documents, Ministry of Civil Aviation; PRS.

The Committee also noted a structural issue in the way airport concessions are given. As of now, entities that bid the highest amount are given the rights to operate an airport. This leads them to pass on the high charge to airline operators. This system does not consider the actual cost of the services and leads to an arbitrary increase in the cost of airline operators. The Ministry sees the role of AAI in future policy issues to include providing high quality, safe and customer-oriented airport and air navigation services. In 2022-23, the government has allocated Rs 150 crore to AAI, which is almost ten times higher than the budget estimates of 2021-22.

Regional Connectivity Scheme (RCS-UDAN)

The top 15 airports in the country account for about 83% of the total passenger traffic. These airports are also close to their saturation limit, and hence the Ministry notes that there is a need to add more Tier-II and Tier-III cities to the aviation network. The Regional Connectivity Scheme was introduced in 2016 to stimulate regional air connectivity and make air travel affordable to the masses. The budget for this scheme is Rs 4,500 crore over five years from 2016-17 to 2021-22. As of December 16, 2021, 46% of this amount has been released. In 2022-23, the scheme has been allocated Rs 601 crore, which is 60% lower than the revised estimates of 2021-22 (Rs 994 crore).

Under the scheme, airline operators are incentivised to operate on under-served routes by providing them with viability gap funding and airport fee waivers. AAI, which is the implementing agency of this scheme, has sanctioned 948 routes to boost regional connectivity. As of January 31, 2022, 43% of these routes have been operationalised. As per the Ministry, lack of availability of land and creation of regional infrastructure has led to delays in the scheme. Issues with obtaining licenses and unsustainable operation of awarded routes also contribute to the delay. As per the Ministry, these issues, along with the setback faced due to the pandemic acted as major obstacles for the effective utilisation of funds.

Figure 3: Expenditure on Regional Connectivity Scheme (in Rs crore)

Note: BE – Budget Estimate; RE – Revised Estimate;

Source: Demand for Grants documents, Ministry of Civil Aviation; PRS.

Potential of air cargo

The Standing Committee on Transport (2021) had noted India’s cargo industry’s huge potential with respect to its geographical location, its growing economy, and its growth in domestic and international trade in the last decade. In 2019-20, all Indian airports together handled 3.33 million metric tonnes (MMT) of freight. This is much lower than the cargo handled by Hong Kong (4.5 MMT), Memphis (4.8 MMT), and Shanghai (3.7 MMT), which are the top three airports in terms of the volume of freight handled. The Standing Committee on Transport (2021) has noted inadequate infrastructure as a major bottleneck in developing the country’s air cargo sector. To reduce such bottleneck, it recommended the Ministry to establish dedicated cargo airports, and automate air cargo procedures and information systems to streamline redundant processes.

The Committee has also highlighted that the Open Sky Policy enables foreign cargo carriers to freely operate cargo services to and from any airports in India having customs/immigration facilities. They account for 90-95% of the total international cargo carried to and from the country. On the other hand, Indian air cargo operators face discriminatory practices and regulatory impediments for operating international cargo flights in foreign countries. The Committee urged the Ministry to provide a level-playing field for Indian air cargo operators and to ensure equal opportunities for them. The Ministry revised the Open Sky Policy in December 2020. Under the revised policy, the operations of foreign ad hoc and pure non-scheduled freighter charter service flights have been restricted to six airports - Bengaluru, Chennai, Delhi, Kolkata, Hyderabad, and Mumbai.

Rising cost of Aviation Turbine Fuel

The cost of Aviation Turbine Fuel (ATF) forms around 40% of the total operating cost of airlines and impacts their financial viability. ATF prices have been consistently rising over the past years, placing stress on the balance sheets of airline companies. As per recent news reports, airfares are expected to rise as the conflict between Russia and Ukraine is making ATF costlier.

ATF attracts VAT which is variable across states and does not have a provision for input tax credit. High rates of aviation fuel coupled with high VAT rates are adversely affecting airline companies.

Table 2: Expenditure on ATF by airlines over the years (in Rs crore)

|

Year |

National Carriers |

Private Domestic Airlines |

|

2016-17 |

7,286 |

10,506 |

|

2017-18 |

8,563 |

13,596 |

|

2018-19 |

11,788 |

20,662 |

|

2019-20 |

11,103 |

23,354 |

|

2020-21 |

3,047 |

7,452 |

Source: Unstarred Question 2581, Rajya Sabha; PRS.

The Ministry, in January 2020, has reduced the tax burden on ATF by eliminating fuel throughput charges that were levied by airport operators at all airports across India. Central excise on ATF was reduced from 14% to 11% w.e.f. October 11, 2018. State governments have also reduced VAT/Sales Tax on ATF drawn on RCS airports to 1% or less for 10 years. For non-RCS-UDAN operations, various state governments have reduced VAT/Sales Tax on ATF to within 5%. The Standing Committee on Transport (2021) has recommended ATF to be included within the ambit of GST and that applicable GST should not exceed 12% on ATF with full Input Tax Credit.

For more details, please refer to the Demand for Grants Analysis of the Ministry of Civil Aviation, 2022-23.