On June 1, 2020, the Cabinet Committee on Economic Affairs approved a revision in the definition of Micro, Small and Medium Enterprises (MSMEs).[1] In this blog, we discuss the change in the definition as approved by the Cabinet, and examine some of the common criteria used for classification of MSMEs.

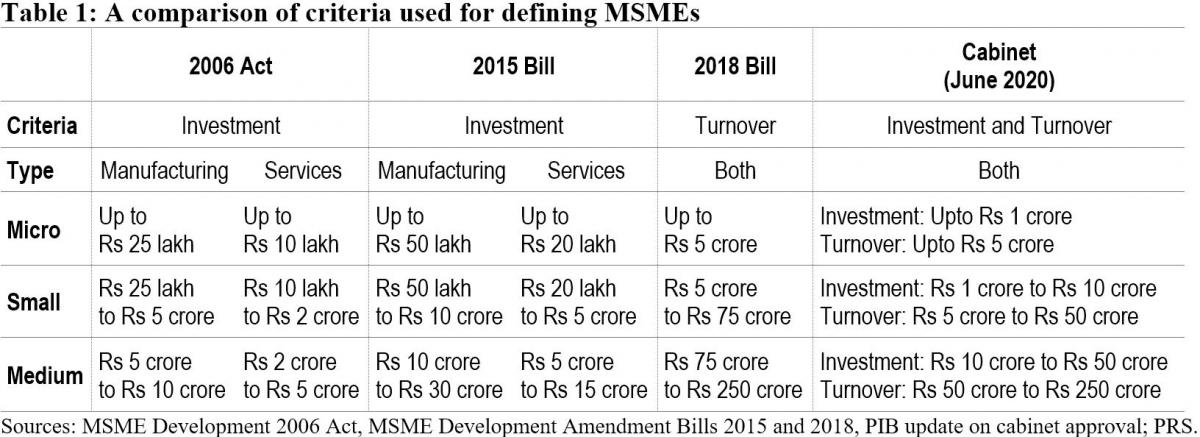

Currently, MSMEs are defined under the Micro, Small and Medium Enterprises Development Act, 2006.[2] The Act classifies them as micro, small and medium enterprises based on: (i) investment in plant and machinery for enterprises engaged in manufacturing or production of goods, and (ii) investment in equipment for enterprises providing services. As per the Cabinet approval, the investment limits will be revised upwards and annual turnover of the enterprise will be used as additional criteria for the classification of MSMEs (Table 1).

Earlier attempts to amend the definition of MSMEs

The central government has sought to revise the definition of MSMEs in the Act on two earlier occasions. The government introduced the MSME Development (Amendment) Bill, 2015 which proposed to increase the investment limits for manufacturing and services MSMEs.[3] This Bill was withdrawn in July 2018 and another Bill was introduced. The MSME Development (Amendment) Bill, 2018 proposed to: (i) use annual turnover as criteria instead of investment for classification of MSMEs, (ii) remove the distinction between manufacturing and services, and (iii) provide the central government with the power to revise the turnover limits, through a notification.[4] The 2018 Bill lapsed with the dissolution of 16th Lok Sabha.

Global trends in criteria for the classification of MSMEs

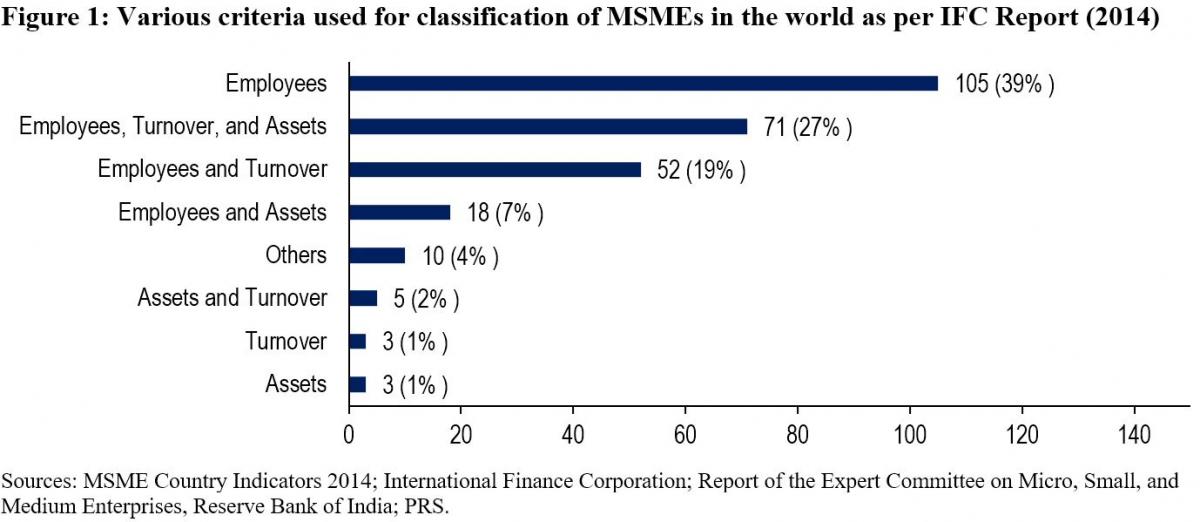

While India will now be using investment and annual turnover as the criteria to classify MSMEs, globally, the number of employees is the most widely used criteria for classifying MSMEs. The Reserve Bank of India's Expert Committee on MSMEs (2019) cited a study by the International Finance Corporation in 2014 which analysed 267 definitions used by different institutions in 155 countries.[5],[6] According to the study, countries used a combination of criteria to classify MSMEs. 92% of the definitions used the number of employees as one of the criteria. Other frequently used criteria were: (i) turnover (49%), and (ii) value of assets (36%). 11% of the analysed definitions used alternative criteria such as: (i) loan size, (ii) years of experience, and (iii) initial investment.

Evaluation of common criteria used to define MSMEs

Investment: The 2006 Act uses investment in plant, machinery, and equipment to classify MSMEs. Some of the issues with the investment criteria include:

Due to their informal and small scale of operations, firms often do not maintain proper books of accounts and hence find it difficult to get classified as MSMEs as per the current definition.5

The investment-based classification incentivises promoters to keep the investment size restricted to retain the benefits associated with the micro or small category.7

Turnover: The 2018 Bill sought to replace the investment criteria with annual turnover as the sole criteria for the classification of MSMEs. The Standing Committee agreed with the proposal under the Bill to use annual turnover as the criteria instead of investment.7 It observed that this could overcome some of the shortcomings of classification based on investment. While turnover based criteria will also require verification, the Committee noted that the GST Network (GSTN) data can act as a reliable source of information for this purpose. However, it also observed that:7

With turnover as a criterion for classification, corporates may misuse the incentives meant for MSMEs. For instance, there is a possibility that a multi-national company may produce a large quantity of products worth a high turnover and then market it through various subsidiaries registered as Micro or Small enterprise under GSTN.

The turnover of some enterprises may fluctuate depending on their business, which may result in the change of classification of the enterprise during a year.

The Committee noted that there is a wide gap in turnover limits. For instance, an enterprise with a turnover of Rs 6 crore and an enterprise with a turnover of Rs 75 crore (as proposed in 2018 Bill) would both be classified as a small enterprise, which seems incongruous.

The Expert Committee (RBI) also recommended using annual turnover as the criteria for classification instead of investment.5 It observed that turnover based definition would be transparent, progressive, and easier to implement through the GSTN. It also recommended that the power to change the definition of MSMEs should be delegated to the executive as it will help in responding to changing economic scenarios.

Number of employees: The Standing Committee had highlighted that in a labour-intensive country like India, appropriate focus is required on employment generation and MSME sector is the most suitable platform for this.7 It had recommended that the central government should assess the number of persons employed in the MSME sector and also consider employment as a criterion while classifying MSMEs. However, the Expert Committee (RBI) stated that while the employment-based definition is an additional feature preferred in some countries, the definition would pose challenges in implementation.5 According to the Ministry of MSME, employment as a criterion has problems due to: (i) factors such as seasonality and informal nature of engagement, (ii) similar to investment criteria, this would also require physical verification and has associated cost overheads.7

Number of MSMEs

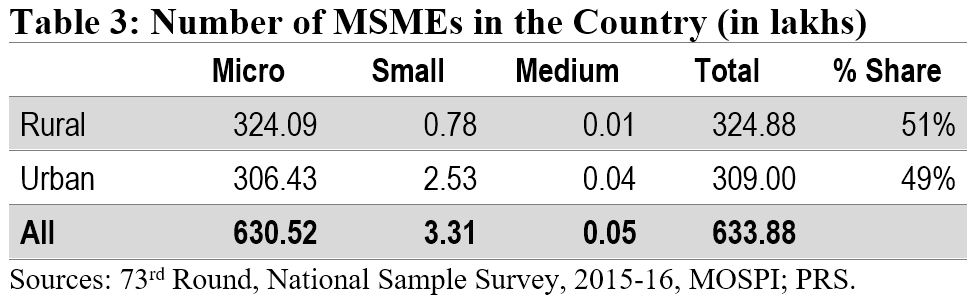

According to the National Sample Survey (2015-16), there were around 6.34 crore MSMEs in the country. The micro sector with 6.3 crore enterprises accounted for more than 99% of the total estimated number of MSMEs. The small and medium sectors accounted for only 0.52% and 0.01% of the estimated number of enterprises, respectively. Another dataset to understand the distribution of MSMEs is Udyog Aadhaar, a unique identity provided by the Unique Identification Authority of India (UIDAI) to MSME enterprises.[8] Udyog Aadhaar registration is based on self-declaration by enterprises. Between September 2015 and June 2020, 98.6 lakh enterprises have registered with UIDAI. According to this dataset, micro, small, and medium enterprises comprise 87.7%, 11.8% and 0.5% of the MSME sector respectively.

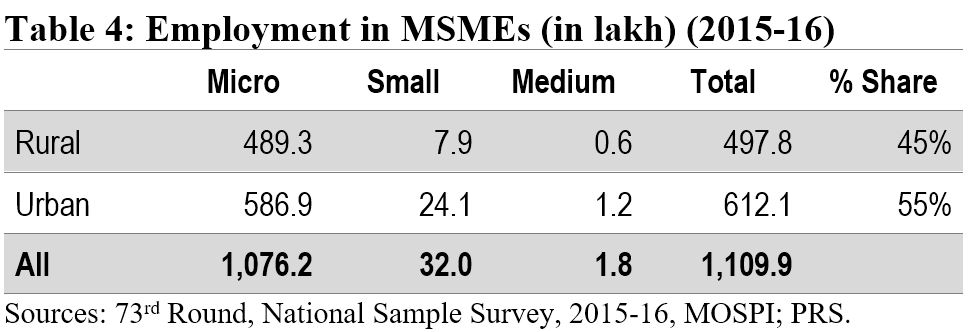

Employment in the MSME sector

The MSME sector employed nearly 11.1 crore people in 2015-16. The sector was the second largest employer after the agriculture sector. The highest number of employed persons were engaged in trade activity (35%), followed by persons engaged in manufacturing (32%).

Implications of change in the definition of MSMEs

The change in the definition of MSMEs may result in many enterprises which are currently classified as Small enterprises be reclassified as Micro, and those classified as Medium enterprises be reclassified as Small. Further, there may be many enterprises which are not currently classified as MSMEs, which may fall under the MSME classification as per the new definition. Such enterprises will also now benefit from the schemes related to MSMEs. The Ministry of MSME runs various schemes to provide for: (i) flow of credit to MSMEs, (ii) support for technology upgrade and modernisation, (iii) entrepreneurship and skill development, and (iv) cluster-wise measures to promote capacity-building and empowerment of MSME units. For instance, under the Credit Guarantee Fund Scheme for Micro and Small Enterprises, a credit guarantee cover of up to 75% of the credit is provided to micro and small enterprises.[9] Thus, the re-classification may require a significant increase in budgetary allocation for the MSME sector.

Other announcements related to MSMEs in the aftermath of COVID-19

MSME sector accounted for nearly 33.4% of the total manufacturing output in 2017-18.[10] During the same year, its share in the country’s total exports was around 49%. Between 2015 and 2017, the contribution of the sector in GDP has been around 30%. Due to the national lockdown induced by COVID-19, businesses including MSMEs have been badly hit. To provide immediate relief to the MSME sector, the government announced several measures in May 2020.[11] These include: (i) collateral-free loans for MSMEs with up to Rs 25 crore outstanding and up to Rs 100 crore turnover, (ii) Rs 20,000 crore as subordinate debt for stressed MSMEs, and (iii) Rs 50,000 crore of capital infusion into MSMEs. These measures have also been approved by the Union Cabinet.[12]

For more details on the announcements made under the Aatma Nirbhar Bharat Abhiyan, see here.

[1] “Cabinet approves Upward revision of MSME definition and modalities/ road map for implementing remaining two Packages for MSMEs (a)Rs 20000 crore package for Distressed MSMEs and (b) Rs 50,000 crore equity infusion through Fund of Funds”, Press Information Bureau, Cabinet Committee on Economic Affairs, June 1, 2020.

[2] The Micro, Small and Medium Enterprises Development Act, 2006, https://samadhaan.msme.gov.in/WriteReadData/DocumentFile/MSMED2006act.pdf.

[3] The Micro, Small and Medium Enterprises Development (Amendment) Bill, 2015, https://www.prsindia.org/sites/default/files/bill_files/MSME_bill%2C_2015_0.pdf.

[4] The Micro, Small and Medium Enterprises Development (Amendment) Bill, 2018, https://www.prsindia.org/sites/default/files/bill_files/The%20Micro%2C%20Small%20and%20Medium%20Enterprises%20Development%20%28Amendment%29%20Bill%2C%202018%20Bill%20Text.pdf.

[5] Report of the Expert Committee on Micro, Small and Medium Enterprises, The Reserve Bank of India, July 2019, https://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/MSMES24062019465CF8CB30594AC29A7A010E8A2A034C.PDF.

[6] MSME Country Indicators 2014, International Finance Corporation, December 2014, https://www.smefinanceforum.org/sites/default/files/analysis%20note.pdf.

[7] 294th Report on Micro Small and Medium Enterprises Development (Amendment) Bill 2018, Standing Committee on Industry, Rajya Sabha, December 2018, https://rajyasabha.nic.in/rsnew/Committee_site/Committee_File/ReportFile/17/111/294_2019_3_15.pdf.

[8] Enterprises with Udyog Aadhaar Number, National Portal for Registration of Micro, Small & Medium Enterprises, Ministry of Micro, Small and Medium Enterprises, https://udyogaadhaar.gov.in/UA/Reports/StateBasedReport_R3.aspx.

[9] Credit Guarantee Fund Scheme for Micro and Small Enterprises, Ministry of Micro, Small and Medium Enterprises, http://www.dcmsme.gov.in/schemes/sccrguarn.htm.

[10] Annual Report 2018-19, Ministry of Micro, Small and Medium Enterprises, https://msme.gov.in/sites/default/files/Annualrprt.pdf.

[11] "Finance Minister announce measures for relief and credit support related to businesses, especially MSMEs to support Indian Economy’s fight against COVID-19", Press Information Bureau, Ministry of Finance, May 13, 2020.

[12] "Cabinet approves additional funding of up to Rupees three lakh crore through introduction of Emergency Credit Line Guarantee Scheme (ECLGS)", Press Information Bureau, Ministry of Finance, May 20, 2020.

This blog has been updated on Jan 19, 2021 to also cover the Madhya Pradesh Ordinance which was promulgated earlier in the month. The comparison table has also been revised accordingly.

On November 27, 2020, the Uttar Pradesh (UP) Prohibition of Unlawful Conversion of Religion Ordinance, 2020 was promulgated by the state government. This was followed by the Madhya Pradesh (MP) government promulgating the Madhya Pradesh Freedom of Religion Ordinance, 2020, in January 2021. These Ordinances seek to regulate religious conversions and prohibit certain types of religious conversions (including through marriages). The MP Ordinance replaces the MP Dharma Swatantra Adhiniyam, 1968, which previously regulated religious conversions in the state. Few other states, including Haryana and Karnataka, are also planning to introduce a similar law. This blog post looks at existing anti-conversion laws in the country and compares the latest UP and MP Ordinances with these laws.

Anti-conversion laws in India

The Constitution guarantees the freedom to profess, propagate, and practise religion, and allows all religious sections to manage their own affairs in matters of religion; subject to public order, morality, and health. To date, there has been no central legislation restricting or regulating religious conversions. Further, in 2015, the Union Law Ministry stated that Parliament does not have the legislative competence to pass anti-conversion legislation. However, it is to be noted that, since 1954, on multiple occasions, Private Member Bills have been introduced in (but never approved by) the Parliament, to regulate religious conversions.

Over the years, several states have enacted ‘Freedom of Religion’ legislation to restrict religious conversions carried out by force, fraud, or inducements. These are: (i) Odisha (1967), (ii) Madhya Pradesh (1968), (iii) Arunachal Pradesh (1978), (iv) Chhattisgarh (2000 and 2006), (v) Gujarat (2003), (vi) Himachal Pradesh (2006 and 2019), (vii) Jharkhand (2017), and (viii) Uttarakhand (2018). Additionally, the Himachal Pradesh (2019) and Uttarakhand legislations also declare a marriage to be void if it was done for the sole purpose of unlawful conversion, or vice-versa. Further, the states of Tamil Nadu (2002) and Rajasthan (2006 and 2008) had also passed similar legislation. However, the Tamil Nadu legislation was repealed in 2006 (after protests by Christian minorities), while in case of Rajasthan, the bills did not receive the Governor’s and President’s assent respectively. Please see Table 2 for a comparison of anti-conversion laws across the country.

In November 2019, citing rising incidents of forced/fraudulent religious conversions, the Uttar Pradesh Law Commission recommended enacting a new law to regulate religious conversions. This led the state government to promulgate the recent Ordinance in 2020. Following UP, the MP government also decided to promulgate an Ordinance in January 2021 to regulate religious conversions. We discuss key features of these ordinances below.

What do the UP and MP Ordinances do?

The MP and UP Ordinances define conversion as renouncing one’s existing religion and adopting another religion. However, both Ordinances exclude re-conversion to immediate previous religion (in UP), and parental religion (in MP) from this definition. Parental religion is the religion to which the individual’s father belonged to, at the time of the individual’s birth. These Ordinances prescribe the procedure for individuals seeking to undergo conversions (in the states of UP and MP) and declare all other forms of conversion (that violate the prescribed procedures) illegal.

Procedure for conversion: Both the Ordinances require: (i) persons wishing to convert to a different religion, and (ii) persons supervising the conversion (religious convertors in UP, and religious priests or persons organising a conversion in MP) to submit an advance declaration of the proposed religious conversion to the District Magistrate (DM). In both states, the individuals seeking to undergo conversion are required to give advance notice of 60 days to the DM. However, in UP, the religious convertors are required to notify one month in advance, whereas in MP, the priests or organisers are also required to notify 60 days in advance. Upon receiving the declarations, the DMs in UP are further required to conduct a police enquiry into the intention, purpose, and cause of the proposed conversion. No such requirement exists in the MP Ordinance, although it mandates the DM’s sanction as a prerequisite for any court to take cognisance of an offence caused by violation of these procedures.

The UP Ordinance also lays down a post-conversion procedure. Post-conversion, within 60 days from the date of conversion, the converted individual is required to submit a declaration (with various personal details) to the DM. The DM will publicly exhibit a copy of the declaration (till the conversion is confirmed) and record any objections to the conversion. The converted individual must then appear before the DM to establish his/her identity, within 21 days of sending the declaration, and confirm the contents of the declaration.

Both the Ordinances also prescribe varying punishments for violation of any procedure prescribed by them, as specified in Table 2.

Prohibition on conversions: Both, the UP and MP Ordinances prohibit conversion of religion through means, such as: (i) force, misrepresentation, undue influence, and allurement, or (ii) fraud, or (iii) marriage. They also prohibit a person from abetting, convincing, and conspiring to such conversions. Further, the Ordinances assign the burden of proof of the lawfulness of religious conversion to: (i) the persons causing or facilitating such conversions, in UP, and (ii) the person accused of causing unlawful conversion, in MP.

Complaints against unlawful conversions: Both Ordinances allow for police complaints, against unlawful religious conversions, to be registered by: (i) the victim of such conversion, (ii) his/her parents or siblings, or (iii) any other person related to them by blood, and marriage or adoption. The MP Ordinance additionally permits persons related by guardianship or custodianship to also register a complaint, provided they take the leave of the court. Further, the MP Ordinance assigns the power to investigate such complaints to police officers of the rank of Sub-Inspector and above.

Marriages involving religious conversion: As per the UP Ordinance, a marriage is liable to be declared null and void, if: (i) it was done for the sole purpose of unlawful conversion, or vice-versa, and (ii) the religious conversion was not done as per the procedure specified in the Ordinance. Similarly, the MP Ordinance declares a marriage null and void, if: (i) it was done with an intent to convert a person, and (ii) the conversion took place through any of the prohibited means specified under the Ordinance. Further, the MP Ordinance explicitly provides for punishment (as specified in Table 2) for the concealment of religion for the purpose of marriage.

Right to inheritance and maintenance: The MP Ordinance additionally provides certain safeguards for women and children. It considers children born out of a marriage involving unlawful religious conversion as legitimate and provides for them to have the right to property of only the father (as per the law governing the inheritance of the father). Further, the Ordinance provides for maintenance to be given to: (i) a woman whose marriage is deemed unlawful under the Ordinance, and (ii) her children born out of such a marriage.

Punishment for unlawful conversions: Both the MP and UP Ordinances provide for punishment for causing or facilitating unlawful religious conversion, as specified in Table 1. Also, all offences under both Ordinances are cognisable and non-bailable.

Additionally, under the UP Ordinance, the accused will be liable to pay compensation of up to five lakh rupees to the victim of conversion and repeat offences will attract double the punishment specified for the respective offence. However, under the MP Ordinance, each repeat offence will attract punishment of a fine, and imprisonment between five and 10 years. Further, it provides for the Session Court to try an accused person, at the same trial, for: (i) an offence under this Ordinance, and (ii) also for other offences he has been charged with, under the Criminal Procedure Code, 1973.

Table 1: Punishments prescribed under the UP and MP Ordinances for offences by individuals for causing/facilitating the conversion

|

Punishment |

Uttar Pradesh |

Madhya Pradesh |

|

Mass conversion (conversion of two or more persons at the same time) |

||

|

Term of imprisonment |

3-10 years |

5-10 years |

|

Fine Amount |

Rs 50,000 or more |

Rs 1,00,000 or more |

|

Conversion of a minor, woman, or person belonging to SC or ST |

||

|

Term of imprisonment |

2-10 years |

2-10 years |

|

Fine Amount |

Rs 25,000 or more |

Rs 50,000 or more |

|

Any other conversion |

||

|

Term of imprisonment |

1-5 years |

1-5 years |

|

Fine Amount |

Rs 15,000 or more |

Rs 25,000 or more |

If any of the above three offences are committed by an organisation, under the UP Ordinance, the registration of the organisation is liable to be cancelled and grants or financial aid from the state government is liable to be discontinued. Under the MP Ordinance, only the registration of such organisations is liable to be cancelled.

* - It is not clear if the Chhattisgarh Law is currently in force or not.

** - Madhya Pradesh originally enacted a law in 1968. And has now replaced it with an Ordinance in 2021.

Note: For Odisha, Jharkhand, and Uttarakhand, some of the penalties have been specified in the Rules published under their respective Acts. For the rest of the states, the penalties have been specified in the respective Acts itself.