The Consumer Protection Bill, 2018 was introduced in Lok Sabha in January 2018. The Bill replaces the Consumer Protection Act, 1986. Previously in 2015, a Bill had been introduced to replace the 1986 Act. The 2015 Bill acknowledged that the rapid change in consumer markets, introduction of practices such as misleading advertisements, and new modes of transactions (online, teleshopping, etc.) had necessitated the need for a new law. The Bill was subsequently referred to a Standing Committee, which recommended several changes to it. The Bill was withdrawn and replaced with the Consumer Protection Bill, 2018. The Bill is listed for passage in the ongoing Monsoon Session. In this post, we analyse the Bill in its current form.

How is the 2018 Bill different from the 1986 Act?

The Bill adds various provisions for consumer protection that were absent in the 1986 Act. Key among them are the provisions on product liability and unfair contracts. Under product liability, when a consumer suffers an injury, property damage or death due to a defect in a product or service, he can file a claim for compensation under product liability. The Bill outlines cases in which the product manufacturer, service provider and seller will be held guilty under product liability. Under the proposed law, to claim product liability, an aggrieved consumer has to prove any one of the conditions mentioned in the Bill with regard to a manufacturer, service provider and seller, as the case may be.

An unfair contract has been defined as a contract between a consumer and manufacturer/ service provider if it causes significant change in consumer rights. Unfair contracts cover six terms, such as payment of excessive security deposits in an arrangement, disproportionate penalty for a breach, and unilateral termination without cause. The consumer courts being set up under the Bill will determine contract terms to be unfair and declare them null and void.

What are the different bodies being set up under the Bill?

The Bill sets up Consumer Protection Councils as advisory bodies, who will advise on protection and promotion of consumer rights. However, it does not make it clear who these Councils will render advise to. Under the 1986 Act, the Consumer Protection Councils have the responsibility to protect and promote consumer rights.

To promote, protect, and enforce consumer rights, the Bill is setting up a regulatory body, known as the Central Consumer Protection Authority. This Authority can also pass orders to prevent unfair and restrictive trade practices, such as selling goods not complying with standards, and impose penalties for false and misleading advertisements.

The Bill also sets up the Consumer Disputes Redressal Commissions (known as consumer courts) at the district, state and national levels. These Commissions will adjudicate a broad range of complaints, including complaints on defective goods and deficient services of varying values. These Commissions are also present under the 1986 Act. However, their pecuniary jurisdiction (amount up to which they can hear complaints) has been revised under the Bill. The Bill also adds a provision for alternate dispute redressal mechanism. As part of this, mediation cells will be attached with the Consumer Disputes Redressal Commissions.

What are the penal provisions under the Bill?

The Bill increases penalties for different offences specified in it. It also adds penalties for offences such as issuing misleading advertisements, and manufacturing and selling adulterated or spurious goods. For example, in case of false and misleading advertisements, the Central Consumer Protection Authority can impose a penalty of up to Rs 10 lakh on a manufacturer or an endorser. For a subsequent offence, the fine may extend to Rs 50 lakh. The manufacturer can also be punished with imprisonment of up to two years, which may extend to five years for every subsequent offence. The Authority can also prohibit the endorser of a misleading advertisement from endorsing any particular product or service for a period of up to one year. For every subsequent offence, the period of prohibition may extend to three years. There are certain exceptions when an endorser will not be held liable for such a penalty.

Are there any issues to think about in the Bill?

The 2018 Bill is a marked improvement over the 2015 Bill and addresses several issues in the 2015 Bill. However, two major issues with regard to the Consumer Disputes Redressal Commissions remain. We discuss them below.

First issue is with regard to the composition of these Commissions. The Bill specifies that the Commissions will be headed by a ‘President’ and will comprise other members. However, the Bill delegates the power of deciding the qualifications of the President and members to the central government. It also does not specify that the President or members should have minimum judicial qualifications. This is in contrast with the existing Consumer Protection Act, 1986, which states that the Commissions at various levels will be headed by a person qualified to be a judge. The 1986 Act also specifies the minimum qualification of members.

Under the current Bill, if the Commissions were to have only non-judicial members, it may violate the principle of separation of powers between the executive and the judiciary. Since these Commissions are adjudicating bodies and will look at consumer dispute cases, it is unclear how a Commission that may comprise only non-judicial members will undertake this function.

Second issue is with regard to the method of appointment of members of the Commissions. The Bill permits the central government to notify the method of appointment of members of the Commissions. It does not require that the selection involve members from the higher judiciary. It may be argued that allowing the executive to determine the appointment of the members of Commissions could affect the independent functioning of the Commissions. This provision is also at variance with the 1986 Act. Under the Act, appointment of members to these Commissions is done through a selection committee. These section committees comprise a judicial member.

As mentioned previously, the Commissions are intended to be quasi-judicial bodies, while the government is part of the executive. There may be instances where the government is a party to a dispute relating to deficiency in service provided by a government enterprise, for e.g., the Railways. In such a case, there would be a conflict of interest as the government would be a party to the dispute before the Commissions and will also have the power to appoint members to the Commission.

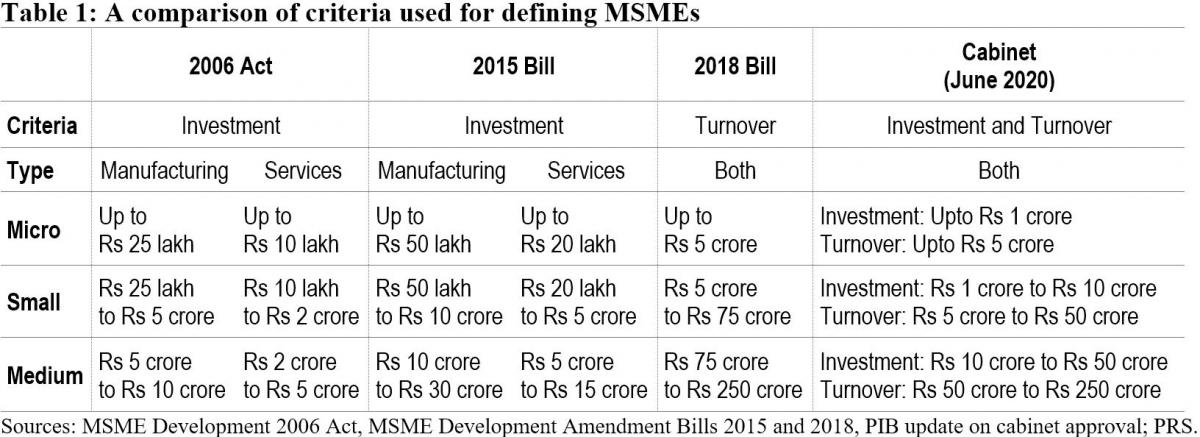

On June 1, 2020, the Cabinet Committee on Economic Affairs approved a revision in the definition of Micro, Small and Medium Enterprises (MSMEs).[1] In this blog, we discuss the change in the definition as approved by the Cabinet, and examine some of the common criteria used for classification of MSMEs.

Currently, MSMEs are defined under the Micro, Small and Medium Enterprises Development Act, 2006.[2] The Act classifies them as micro, small and medium enterprises based on: (i) investment in plant and machinery for enterprises engaged in manufacturing or production of goods, and (ii) investment in equipment for enterprises providing services. As per the Cabinet approval, the investment limits will be revised upwards and annual turnover of the enterprise will be used as additional criteria for the classification of MSMEs (Table 1).

Earlier attempts to amend the definition of MSMEs

The central government has sought to revise the definition of MSMEs in the Act on two earlier occasions. The government introduced the MSME Development (Amendment) Bill, 2015 which proposed to increase the investment limits for manufacturing and services MSMEs.[3] This Bill was withdrawn in July 2018 and another Bill was introduced. The MSME Development (Amendment) Bill, 2018 proposed to: (i) use annual turnover as criteria instead of investment for classification of MSMEs, (ii) remove the distinction between manufacturing and services, and (iii) provide the central government with the power to revise the turnover limits, through a notification.[4] The 2018 Bill lapsed with the dissolution of 16th Lok Sabha.

Global trends in criteria for the classification of MSMEs

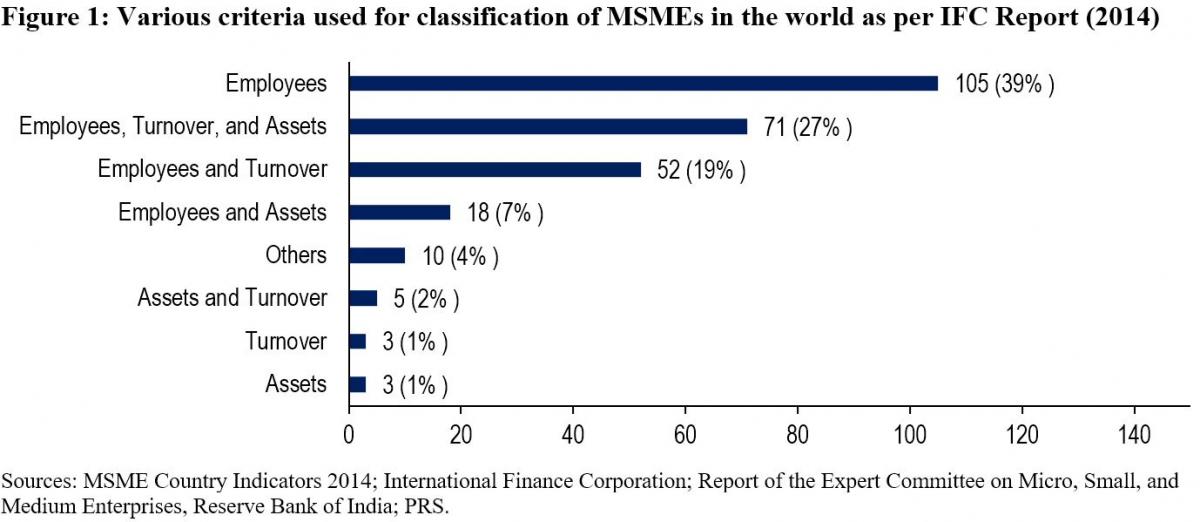

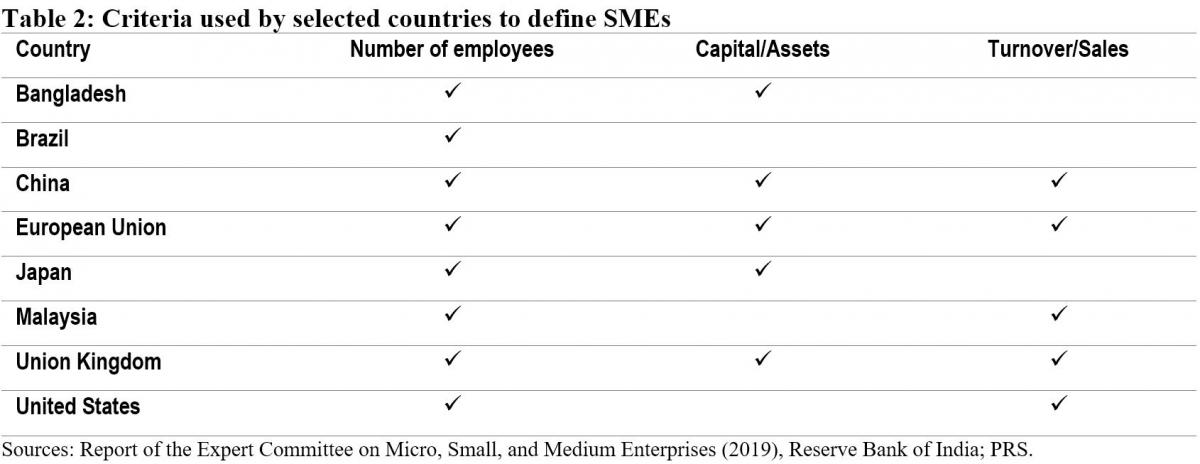

While India will now be using investment and annual turnover as the criteria to classify MSMEs, globally, the number of employees is the most widely used criteria for classifying MSMEs. The Reserve Bank of India's Expert Committee on MSMEs (2019) cited a study by the International Finance Corporation in 2014 which analysed 267 definitions used by different institutions in 155 countries.[5],[6] According to the study, countries used a combination of criteria to classify MSMEs. 92% of the definitions used the number of employees as one of the criteria. Other frequently used criteria were: (i) turnover (49%), and (ii) value of assets (36%). 11% of the analysed definitions used alternative criteria such as: (i) loan size, (ii) years of experience, and (iii) initial investment.

Evaluation of common criteria used to define MSMEs

Investment: The 2006 Act uses investment in plant, machinery, and equipment to classify MSMEs. Some of the issues with the investment criteria include:

Due to their informal and small scale of operations, firms often do not maintain proper books of accounts and hence find it difficult to get classified as MSMEs as per the current definition.5

The investment-based classification incentivises promoters to keep the investment size restricted to retain the benefits associated with the micro or small category.7

Turnover: The 2018 Bill sought to replace the investment criteria with annual turnover as the sole criteria for the classification of MSMEs. The Standing Committee agreed with the proposal under the Bill to use annual turnover as the criteria instead of investment.7 It observed that this could overcome some of the shortcomings of classification based on investment. While turnover based criteria will also require verification, the Committee noted that the GST Network (GSTN) data can act as a reliable source of information for this purpose. However, it also observed that:7

With turnover as a criterion for classification, corporates may misuse the incentives meant for MSMEs. For instance, there is a possibility that a multi-national company may produce a large quantity of products worth a high turnover and then market it through various subsidiaries registered as Micro or Small enterprise under GSTN.

The turnover of some enterprises may fluctuate depending on their business, which may result in the change of classification of the enterprise during a year.

The Committee noted that there is a wide gap in turnover limits. For instance, an enterprise with a turnover of Rs 6 crore and an enterprise with a turnover of Rs 75 crore (as proposed in 2018 Bill) would both be classified as a small enterprise, which seems incongruous.

The Expert Committee (RBI) also recommended using annual turnover as the criteria for classification instead of investment.5 It observed that turnover based definition would be transparent, progressive, and easier to implement through the GSTN. It also recommended that the power to change the definition of MSMEs should be delegated to the executive as it will help in responding to changing economic scenarios.

Number of employees: The Standing Committee had highlighted that in a labour-intensive country like India, appropriate focus is required on employment generation and MSME sector is the most suitable platform for this.7 It had recommended that the central government should assess the number of persons employed in the MSME sector and also consider employment as a criterion while classifying MSMEs. However, the Expert Committee (RBI) stated that while the employment-based definition is an additional feature preferred in some countries, the definition would pose challenges in implementation.5 According to the Ministry of MSME, employment as a criterion has problems due to: (i) factors such as seasonality and informal nature of engagement, (ii) similar to investment criteria, this would also require physical verification and has associated cost overheads.7

Number of MSMEs

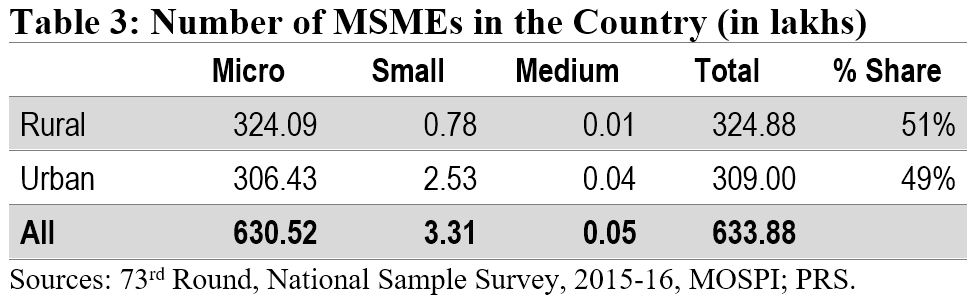

According to the National Sample Survey (2015-16), there were around 6.34 crore MSMEs in the country. The micro sector with 6.3 crore enterprises accounted for more than 99% of the total estimated number of MSMEs. The small and medium sectors accounted for only 0.52% and 0.01% of the estimated number of enterprises, respectively. Another dataset to understand the distribution of MSMEs is Udyog Aadhaar, a unique identity provided by the Unique Identification Authority of India (UIDAI) to MSME enterprises.[8] Udyog Aadhaar registration is based on self-declaration by enterprises. Between September 2015 and June 2020, 98.6 lakh enterprises have registered with UIDAI. According to this dataset, micro, small, and medium enterprises comprise 87.7%, 11.8% and 0.5% of the MSME sector respectively.

Employment in the MSME sector

The MSME sector employed nearly 11.1 crore people in 2015-16. The sector was the second largest employer after the agriculture sector. The highest number of employed persons were engaged in trade activity (35%), followed by persons engaged in manufacturing (32%).

Implications of change in the definition of MSMEs

The change in the definition of MSMEs may result in many enterprises which are currently classified as Small enterprises be reclassified as Micro, and those classified as Medium enterprises be reclassified as Small. Further, there may be many enterprises which are not currently classified as MSMEs, which may fall under the MSME classification as per the new definition. Such enterprises will also now benefit from the schemes related to MSMEs. The Ministry of MSME runs various schemes to provide for: (i) flow of credit to MSMEs, (ii) support for technology upgrade and modernisation, (iii) entrepreneurship and skill development, and (iv) cluster-wise measures to promote capacity-building and empowerment of MSME units. For instance, under the Credit Guarantee Fund Scheme for Micro and Small Enterprises, a credit guarantee cover of up to 75% of the credit is provided to micro and small enterprises.[9] Thus, the re-classification may require a significant increase in budgetary allocation for the MSME sector.

Other announcements related to MSMEs in the aftermath of COVID-19

MSME sector accounted for nearly 33.4% of the total manufacturing output in 2017-18.[10] During the same year, its share in the country’s total exports was around 49%. Between 2015 and 2017, the contribution of the sector in GDP has been around 30%. Due to the national lockdown induced by COVID-19, businesses including MSMEs have been badly hit. To provide immediate relief to the MSME sector, the government announced several measures in May 2020.[11] These include: (i) collateral-free loans for MSMEs with up to Rs 25 crore outstanding and up to Rs 100 crore turnover, (ii) Rs 20,000 crore as subordinate debt for stressed MSMEs, and (iii) Rs 50,000 crore of capital infusion into MSMEs. These measures have also been approved by the Union Cabinet.[12]

For more details on the announcements made under the Aatma Nirbhar Bharat Abhiyan, see here.

[1] “Cabinet approves Upward revision of MSME definition and modalities/ road map for implementing remaining two Packages for MSMEs (a)Rs 20000 crore package for Distressed MSMEs and (b) Rs 50,000 crore equity infusion through Fund of Funds”, Press Information Bureau, Cabinet Committee on Economic Affairs, June 1, 2020.

[2] The Micro, Small and Medium Enterprises Development Act, 2006, https://samadhaan.msme.gov.in/WriteReadData/DocumentFile/MSMED2006act.pdf.

[3] The Micro, Small and Medium Enterprises Development (Amendment) Bill, 2015, https://www.prsindia.org/sites/default/files/bill_files/MSME_bill%2C_2015_0.pdf.

[4] The Micro, Small and Medium Enterprises Development (Amendment) Bill, 2018, https://www.prsindia.org/sites/default/files/bill_files/The%20Micro%2C%20Small%20and%20Medium%20Enterprises%20Development%20%28Amendment%29%20Bill%2C%202018%20Bill%20Text.pdf.

[5] Report of the Expert Committee on Micro, Small and Medium Enterprises, The Reserve Bank of India, July 2019, https://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/MSMES24062019465CF8CB30594AC29A7A010E8A2A034C.PDF.

[6] MSME Country Indicators 2014, International Finance Corporation, December 2014, https://www.smefinanceforum.org/sites/default/files/analysis%20note.pdf.

[7] 294th Report on Micro Small and Medium Enterprises Development (Amendment) Bill 2018, Standing Committee on Industry, Rajya Sabha, December 2018, https://rajyasabha.nic.in/rsnew/Committee_site/Committee_File/ReportFile/17/111/294_2019_3_15.pdf.

[8] Enterprises with Udyog Aadhaar Number, National Portal for Registration of Micro, Small & Medium Enterprises, Ministry of Micro, Small and Medium Enterprises, https://udyogaadhaar.gov.in/UA/Reports/StateBasedReport_R3.aspx.

[9] Credit Guarantee Fund Scheme for Micro and Small Enterprises, Ministry of Micro, Small and Medium Enterprises, http://www.dcmsme.gov.in/schemes/sccrguarn.htm.

[10] Annual Report 2018-19, Ministry of Micro, Small and Medium Enterprises, https://msme.gov.in/sites/default/files/Annualrprt.pdf.

[11] "Finance Minister announce measures for relief and credit support related to businesses, especially MSMEs to support Indian Economy’s fight against COVID-19", Press Information Bureau, Ministry of Finance, May 13, 2020.

[12] "Cabinet approves additional funding of up to Rupees three lakh crore through introduction of Emergency Credit Line Guarantee Scheme (ECLGS)", Press Information Bureau, Ministry of Finance, May 20, 2020.