The 15th Lok Sabha is close to the end of its tenure. A key legislation that proposes major reforms in food security was listed for discussion in Parliament. The National Food Security Bill, 2011 has been scrutinised by a Standing Committee. In January, we compared the Standing Committee's recommendations with the provisions of the Bill. Since then, amendments to the Bill have been introduced in Parliament. Debates on the Bill have revolved around the method of delivering food security, the identification of beneficiaries and the financial implications of the Bill. Method of delivery The Bill aims to make the right to food a statutory right. It proposes to use the existing Public Distribution System (PDS) to deliver foodgrain to 75% of the rural and 50% of the urban population. However, the Bill also allows for cash transfers and food coupons in lieu of grains as mechanisms to deliver food security. While the PDS is known to suffer from leakages as high as 40%, cash transfers and food coupons are known to expose recipients to volatility and price inflation. Each method of delivery would have its own implications, financial and otherwise. The table below compares these methods of delivery.[i] [table id=7 /]

Identification The Bill does not universalise food entitlements. It classifies the population into two categories of beneficiaries, who shall be identified by the centre and states. Mechanisms that aim to target benefits to certain sections of the population have been prone to large inclusion and exclusion errors. A 2009 expert group study headed by N.C. Saxena that evaluated PDS, estimated that about 61% of the eligible population was excluded from the BPL list while 25% of APL households were included in the BPL list. Beneficiaries under the Food Security Bill will be identified through a similar process. It is unclear how these errors in identification of beneficiaries under the PDS will be addressed by the Bill. Financial implications - cost sharing between the centre and states A Bill that aims to deliver food security to a large section of the country would have significant financial implications. Costs shall be shared between the centre and states. Costs imposed on states (partial or full) include: nutritional support to pregnant women and lactating mothers, mid-day meals, anganwadi infrastructure, meals for children suffering from malnutrition, transport and delivery of foodgrains, creating and maintaining storage facilities, and costs associated with District Grievance Redressal Officers and State Food Commissions. Although the centre shall provide some assistance, states will have to bear a significant financial burden on account of implementation. It is unclear whether Parliament can require states to allocate funds without encroaching on the powers of state legislative assemblies. If a state chooses not to allocate the necessary funds or does not possess the funds to do so, implementation of the Bill could be seriously affected. The Standing Committee examining the Bill had recommended that an independent body, such as the Finance Commission, should be consulted regarding additional funds to be borne by states. The Right to Education Act with similar centre-state sharing of funds provides for such a consultation with the Finance Commission. Cost of implementation of the Bill Another contentious issue is the cost of implementing the Bill. The Bill estimates the cost at Rs 95,000 crore. However, experts have made varying estimates on the costs ranging from Rs 2 lakh crore to Rs 3.5 lakh crore. Ashok Gulati, Chairman of the Commission for Agricultural Costs and Prices, estimated the cost at 2 lakh crore per year whereas the Minister of Food, K.V. Thomas was reported to have estimated the cost at Rs 3.5 lakh crore. The passage of the food security Bill in Parliament will depend on the ability of the government to build consensus on these issues. It remains to be seen how the Bill is debated next Parliament session.

[i] Kapur D., Mukhopadhyay P., and A. Subramanian. “The Case for Direct Cash Transfers to the Poor.” Economic and Political Weekly. Vol 43, No 15 (Apr 12-18, 2008). Khera, R. “Revival of the Public Distribution System: Evidence and Explanations.” Economic and Political Weekly. Vol XLVI, Nos 44 & 45 (Nov 5, 2011). Shah, M. “Direct Cash Transfers: No Magic Bullet.” Economic and Political Weekly. Vol 43, No 34, pp. 77-79 (Aug 23-29, 2008).

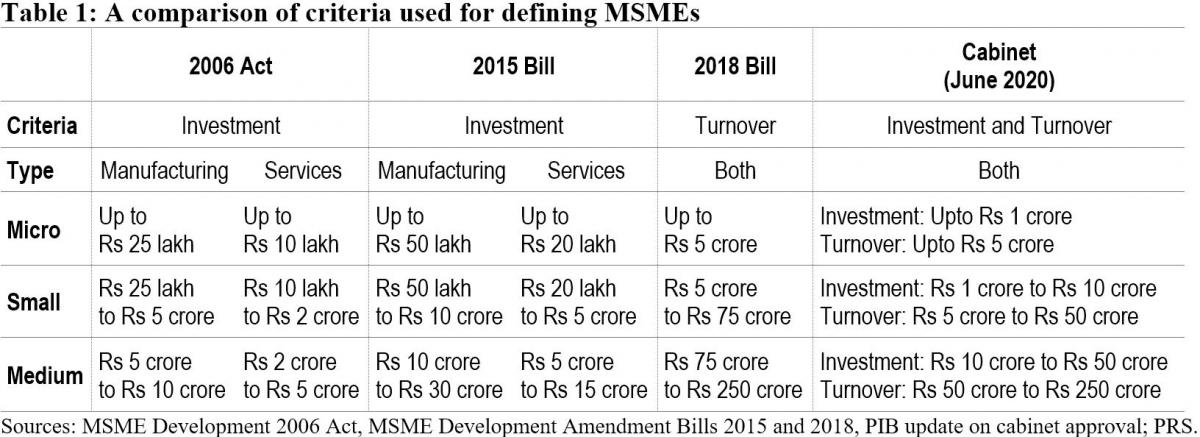

On June 1, 2020, the Cabinet Committee on Economic Affairs approved a revision in the definition of Micro, Small and Medium Enterprises (MSMEs).[1] In this blog, we discuss the change in the definition as approved by the Cabinet, and examine some of the common criteria used for classification of MSMEs.

Currently, MSMEs are defined under the Micro, Small and Medium Enterprises Development Act, 2006.[2] The Act classifies them as micro, small and medium enterprises based on: (i) investment in plant and machinery for enterprises engaged in manufacturing or production of goods, and (ii) investment in equipment for enterprises providing services. As per the Cabinet approval, the investment limits will be revised upwards and annual turnover of the enterprise will be used as additional criteria for the classification of MSMEs (Table 1).

Earlier attempts to amend the definition of MSMEs

The central government has sought to revise the definition of MSMEs in the Act on two earlier occasions. The government introduced the MSME Development (Amendment) Bill, 2015 which proposed to increase the investment limits for manufacturing and services MSMEs.[3] This Bill was withdrawn in July 2018 and another Bill was introduced. The MSME Development (Amendment) Bill, 2018 proposed to: (i) use annual turnover as criteria instead of investment for classification of MSMEs, (ii) remove the distinction between manufacturing and services, and (iii) provide the central government with the power to revise the turnover limits, through a notification.[4] The 2018 Bill lapsed with the dissolution of 16th Lok Sabha.

Global trends in criteria for the classification of MSMEs

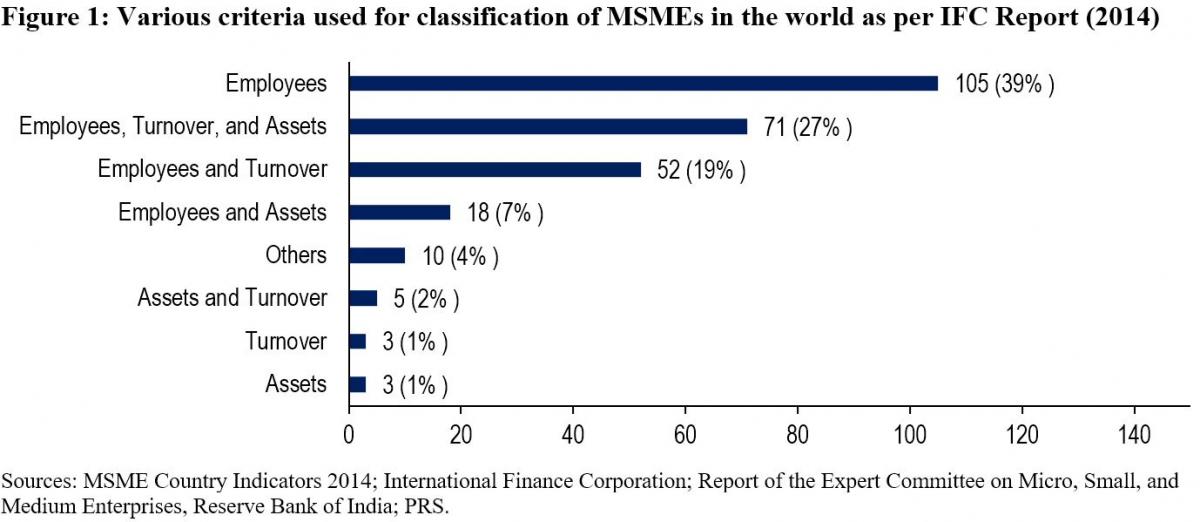

While India will now be using investment and annual turnover as the criteria to classify MSMEs, globally, the number of employees is the most widely used criteria for classifying MSMEs. The Reserve Bank of India's Expert Committee on MSMEs (2019) cited a study by the International Finance Corporation in 2014 which analysed 267 definitions used by different institutions in 155 countries.[5],[6] According to the study, countries used a combination of criteria to classify MSMEs. 92% of the definitions used the number of employees as one of the criteria. Other frequently used criteria were: (i) turnover (49%), and (ii) value of assets (36%). 11% of the analysed definitions used alternative criteria such as: (i) loan size, (ii) years of experience, and (iii) initial investment.

Evaluation of common criteria used to define MSMEs

Investment: The 2006 Act uses investment in plant, machinery, and equipment to classify MSMEs. Some of the issues with the investment criteria include:

Due to their informal and small scale of operations, firms often do not maintain proper books of accounts and hence find it difficult to get classified as MSMEs as per the current definition.5

The investment-based classification incentivises promoters to keep the investment size restricted to retain the benefits associated with the micro or small category.7

Turnover: The 2018 Bill sought to replace the investment criteria with annual turnover as the sole criteria for the classification of MSMEs. The Standing Committee agreed with the proposal under the Bill to use annual turnover as the criteria instead of investment.7 It observed that this could overcome some of the shortcomings of classification based on investment. While turnover based criteria will also require verification, the Committee noted that the GST Network (GSTN) data can act as a reliable source of information for this purpose. However, it also observed that:7

With turnover as a criterion for classification, corporates may misuse the incentives meant for MSMEs. For instance, there is a possibility that a multi-national company may produce a large quantity of products worth a high turnover and then market it through various subsidiaries registered as Micro or Small enterprise under GSTN.

The turnover of some enterprises may fluctuate depending on their business, which may result in the change of classification of the enterprise during a year.

The Committee noted that there is a wide gap in turnover limits. For instance, an enterprise with a turnover of Rs 6 crore and an enterprise with a turnover of Rs 75 crore (as proposed in 2018 Bill) would both be classified as a small enterprise, which seems incongruous.

The Expert Committee (RBI) also recommended using annual turnover as the criteria for classification instead of investment.5 It observed that turnover based definition would be transparent, progressive, and easier to implement through the GSTN. It also recommended that the power to change the definition of MSMEs should be delegated to the executive as it will help in responding to changing economic scenarios.

Number of employees: The Standing Committee had highlighted that in a labour-intensive country like India, appropriate focus is required on employment generation and MSME sector is the most suitable platform for this.7 It had recommended that the central government should assess the number of persons employed in the MSME sector and also consider employment as a criterion while classifying MSMEs. However, the Expert Committee (RBI) stated that while the employment-based definition is an additional feature preferred in some countries, the definition would pose challenges in implementation.5 According to the Ministry of MSME, employment as a criterion has problems due to: (i) factors such as seasonality and informal nature of engagement, (ii) similar to investment criteria, this would also require physical verification and has associated cost overheads.7

Number of MSMEs

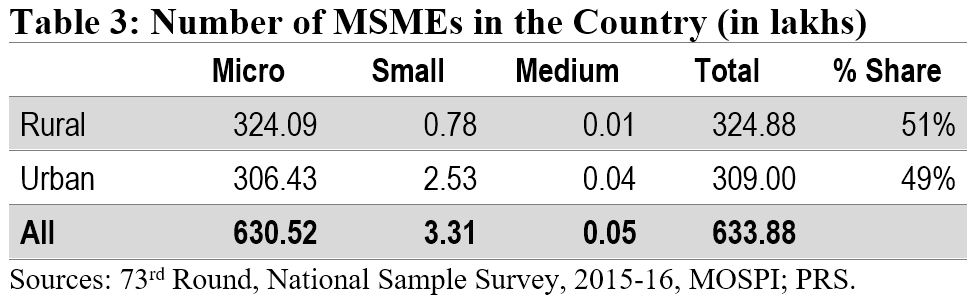

According to the National Sample Survey (2015-16), there were around 6.34 crore MSMEs in the country. The micro sector with 6.3 crore enterprises accounted for more than 99% of the total estimated number of MSMEs. The small and medium sectors accounted for only 0.52% and 0.01% of the estimated number of enterprises, respectively. Another dataset to understand the distribution of MSMEs is Udyog Aadhaar, a unique identity provided by the Unique Identification Authority of India (UIDAI) to MSME enterprises.[8] Udyog Aadhaar registration is based on self-declaration by enterprises. Between September 2015 and June 2020, 98.6 lakh enterprises have registered with UIDAI. According to this dataset, micro, small, and medium enterprises comprise 87.7%, 11.8% and 0.5% of the MSME sector respectively.

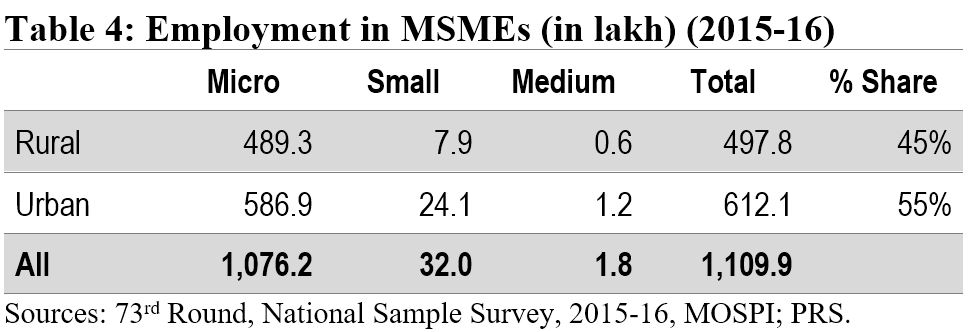

Employment in the MSME sector

The MSME sector employed nearly 11.1 crore people in 2015-16. The sector was the second largest employer after the agriculture sector. The highest number of employed persons were engaged in trade activity (35%), followed by persons engaged in manufacturing (32%).

Implications of change in the definition of MSMEs

The change in the definition of MSMEs may result in many enterprises which are currently classified as Small enterprises be reclassified as Micro, and those classified as Medium enterprises be reclassified as Small. Further, there may be many enterprises which are not currently classified as MSMEs, which may fall under the MSME classification as per the new definition. Such enterprises will also now benefit from the schemes related to MSMEs. The Ministry of MSME runs various schemes to provide for: (i) flow of credit to MSMEs, (ii) support for technology upgrade and modernisation, (iii) entrepreneurship and skill development, and (iv) cluster-wise measures to promote capacity-building and empowerment of MSME units. For instance, under the Credit Guarantee Fund Scheme for Micro and Small Enterprises, a credit guarantee cover of up to 75% of the credit is provided to micro and small enterprises.[9] Thus, the re-classification may require a significant increase in budgetary allocation for the MSME sector.

Other announcements related to MSMEs in the aftermath of COVID-19

MSME sector accounted for nearly 33.4% of the total manufacturing output in 2017-18.[10] During the same year, its share in the country’s total exports was around 49%. Between 2015 and 2017, the contribution of the sector in GDP has been around 30%. Due to the national lockdown induced by COVID-19, businesses including MSMEs have been badly hit. To provide immediate relief to the MSME sector, the government announced several measures in May 2020.[11] These include: (i) collateral-free loans for MSMEs with up to Rs 25 crore outstanding and up to Rs 100 crore turnover, (ii) Rs 20,000 crore as subordinate debt for stressed MSMEs, and (iii) Rs 50,000 crore of capital infusion into MSMEs. These measures have also been approved by the Union Cabinet.[12]

For more details on the announcements made under the Aatma Nirbhar Bharat Abhiyan, see here.

[1] “Cabinet approves Upward revision of MSME definition and modalities/ road map for implementing remaining two Packages for MSMEs (a)Rs 20000 crore package for Distressed MSMEs and (b) Rs 50,000 crore equity infusion through Fund of Funds”, Press Information Bureau, Cabinet Committee on Economic Affairs, June 1, 2020.

[2] The Micro, Small and Medium Enterprises Development Act, 2006, https://samadhaan.msme.gov.in/WriteReadData/DocumentFile/MSMED2006act.pdf.

[3] The Micro, Small and Medium Enterprises Development (Amendment) Bill, 2015, https://www.prsindia.org/sites/default/files/bill_files/MSME_bill%2C_2015_0.pdf.

[4] The Micro, Small and Medium Enterprises Development (Amendment) Bill, 2018, https://www.prsindia.org/sites/default/files/bill_files/The%20Micro%2C%20Small%20and%20Medium%20Enterprises%20Development%20%28Amendment%29%20Bill%2C%202018%20Bill%20Text.pdf.

[5] Report of the Expert Committee on Micro, Small and Medium Enterprises, The Reserve Bank of India, July 2019, https://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/MSMES24062019465CF8CB30594AC29A7A010E8A2A034C.PDF.

[6] MSME Country Indicators 2014, International Finance Corporation, December 2014, https://www.smefinanceforum.org/sites/default/files/analysis%20note.pdf.

[7] 294th Report on Micro Small and Medium Enterprises Development (Amendment) Bill 2018, Standing Committee on Industry, Rajya Sabha, December 2018, https://rajyasabha.nic.in/rsnew/Committee_site/Committee_File/ReportFile/17/111/294_2019_3_15.pdf.

[8] Enterprises with Udyog Aadhaar Number, National Portal for Registration of Micro, Small & Medium Enterprises, Ministry of Micro, Small and Medium Enterprises, https://udyogaadhaar.gov.in/UA/Reports/StateBasedReport_R3.aspx.

[9] Credit Guarantee Fund Scheme for Micro and Small Enterprises, Ministry of Micro, Small and Medium Enterprises, http://www.dcmsme.gov.in/schemes/sccrguarn.htm.

[10] Annual Report 2018-19, Ministry of Micro, Small and Medium Enterprises, https://msme.gov.in/sites/default/files/Annualrprt.pdf.

[11] "Finance Minister announce measures for relief and credit support related to businesses, especially MSMEs to support Indian Economy’s fight against COVID-19", Press Information Bureau, Ministry of Finance, May 13, 2020.

[12] "Cabinet approves additional funding of up to Rupees three lakh crore through introduction of Emergency Credit Line Guarantee Scheme (ECLGS)", Press Information Bureau, Ministry of Finance, May 20, 2020.