The Financial Resolution and Deposit Insurance Bill, 2017 was introduced in Parliament during Monsoon Session 2017.[1] The Bill proposes to create a framework for monitoring financial firms such as banks, insurance companies, and stock exchanges; pre-empt risk to their financial position; and resolve them if they fail to honour their obligations (such as repaying depositors). To ensure continuity of a failing firm, it may be resolved by merging it with another firm, transferring its assets and liabilities, or reducing its debt. If resolution is found to be unviable, the firm may be liquidated, and its assets sold to repay its creditors.

After introduction, the Bill was referred to a Joint Committee of Parliament for examination, and the Committee’s report is expected in the Winter Session 2017. The Committee has been inviting stakeholders to give their inputs on the Bill, consulting experts, and undertaking study tours. In this context, we discuss the provisions of the Bill and some issues for consideration.

What are financial firms?

Financial firms include banks, insurance companies, and stock exchanges, among others. These firms accept deposits from consumers, channel these deposits into investments, provide loans, and manage payment systems that facilitate transactions in the country. These firms are an integral part of the financial system, and since they transact with each other, their failure may have an adverse impact on financial stability and result in consumers losing their deposits and investments.

As witnessed in 2008, the failure of a firm (Lehman Brothers) impacted the financial system across the world, and triggered a global financial crisis. After the crisis, various countries have sought to consolidate their laws to develop specialised capabilities for resolving failure of financial firms and to prevent the occurrence of another crisis. [2]

What is the current framework to resolve financial firms? What does the Bill propose?

Currently, there is no specialised law for the resolution of financial firms in India. Provisions to resolve failure of financial firms are found scattered across different laws.2 Resolution or winding up of firms is managed by the regulators for various kinds of financial firms (i.e. the Reserve Bank of India (RBI) for banks, the Insurance Regulatory and Development Authority (IRDA) for insurance companies, and the Securities and Exchange Board of India (SEBI) for stock exchanges.) However, under the current framework, powers of these regulators to resolve similar entities may vary (e.g. RBI has powers to wind-up or merge scheduled commercial banks, but not co-operative banks.)

The Bill seeks to create a consolidated framework for the resolution of financial firms by creating a Resolution Corporation. The Resolution Corporation will include representatives from all financial sector regulators and the ministry of finance, among others. The Corporation will monitor these firms to pre-empt failure, and resolve or liquidate them in case of such failure.

How does the Resolution Corporation monitor and prevent failure of financial firms?

Risk based classification: The Resolution Corporation or the regulators (such as the RBI for banks, IRDA for insurance companies or SEBI for the stock exchanges) will classify financial firms under five categories, based on their risk of failure (see Figure 1). This classification will be based on adequacy of capital, assets and liabilities, and capability of management, among other criteria. The Bill proposes to allow both, the regulator and the Corporation, to monitor and classify firms based on their risk to failure.

Corrective Action: Based on the risk to failure, the Resolution Corporation or regulators may direct the firms to take certain corrective action. For example, if the firm is at a higher risk to failure (under ‘material’ or ‘imminent’ categories), the Resolution Corporation or the regulator may: (i) prevent it from accepting deposits from consumers, (ii) prohibit the firm from acquiring other businesses, or (iii) require it to increase its capital. Further, these firms will formulate resolution and restoration plans to prepare a strategy for improving their financial position and resolving the firm in case it fails.

While the Bill specifies that the financial firms will be classified based on risk, it does not provide a mechanism for these firms to appeal this decision. One argument to not allow an appeal may be that certain decisions of the Corporation may require urgent action to prevent the financial firm from failing. However, this may leave aggrieved persons without a recourse to challenge the decision of the Corporation if they are unsatisfied.

Figure 1: Monitoring and resolution of financial firms

How will the Resolution Corporation resolve financial firms that have failed?

The Resolution Corporation will take over the administration of a financial firm from the date of its classification as ‘critical’ (i.e. if it is on the verge of failure.) The Resolution Corporation will resolve the firm using any of the methods specified in the Bill, within one year. This time limit may be extended by another year (i.e. maximum limit of two years). During this period, the firm will be immune against all legal actions.

The Resolution Corporation can resolve a financial firm using any of the following methods: (i) transferring the assets and liabilities of the firm to another firm, (ii) merger or acquisition of the firm, (iii) creating a bridge financial firm (where a new company is created to take over the assets, liabilities and management of the failing firm), (iv) bail-in (internally transferring or converting the debt of the firm), or (v) liquidate the firm to repay its creditors.

If the Resolution Corporation fails to resolve the firm within a maximum period of two years, the firm will automatically go in for liquidation. The Bill specifies the order of priority in which creditors will be repaid in case of liquidation, with the amount paid to depositors as deposit insurance getting preference over other creditors.

While the Bill specifies that resolution will commence upon classification as ‘critical’, the point at which this process will end may not be evident in certain cases. For example, in case of transfer, merger or liquidation, the end of the process may be inferred from when the operations are transferred or liquidation is completed, but for some other methods such as bail-in, the point at which the resolution process will be completed may be unclear.

Does the Bill guarantee the repayment of bank deposits?

The Resolution Corporation will provide deposit insurance to banks up to a certain limit. This implies, that the Corporation will guarantee the repayment of a certain amount to each depositor in case the bank fails. Currently, the Deposit Insurance and Credit Guarantee Corporation (DICGC) provides deposit insurance for bank deposits up to 1 lakh rupees per depositor.[3] The Bill proposes to subsume the functions of the DICGC under the Resolution Corporation.

[1]. The Financial Resolution and Deposit Insurance Bill, 2017, http://www.prsindia.org/uploads/media/Financial%20Resolution%20Bill,%202017/Financial%20Resolution%20Bill,%202017.pdf

[2]. Report of the Committee to Draft Code on Resolution of Financial Firms, September 2016, http://www.prsindia.org/uploads/media/Financial%20Resolution%20Bill,%202017/FRDI%20Bill%20Drafting%20Committee%20Report.pdf

[3]. The Deposit Insurance and Credit Guarantee Corporation Act, 1961, http://www.prsindia.org/uploads/media/Financial%20Resolution%20Bill,%202017/DICGC%20Act,%

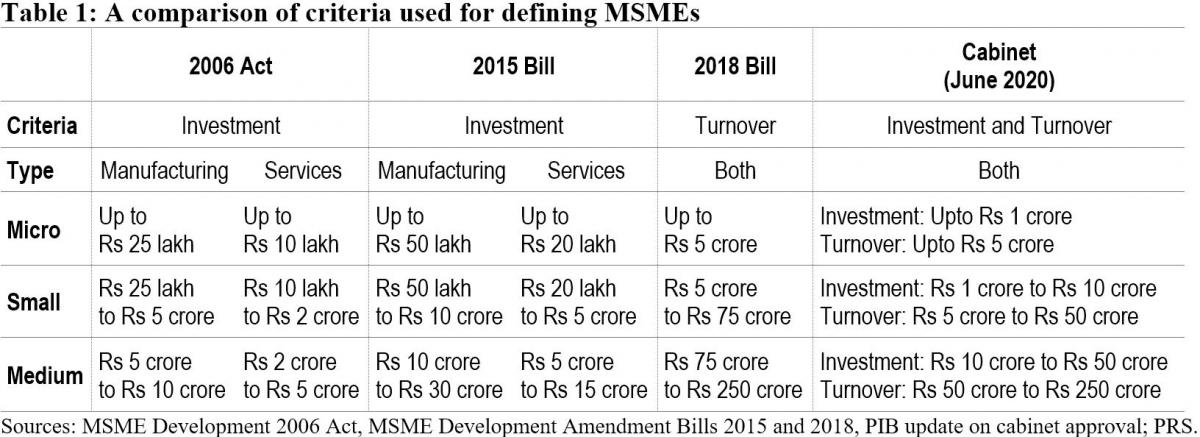

On June 1, 2020, the Cabinet Committee on Economic Affairs approved a revision in the definition of Micro, Small and Medium Enterprises (MSMEs).[1] In this blog, we discuss the change in the definition as approved by the Cabinet, and examine some of the common criteria used for classification of MSMEs.

Currently, MSMEs are defined under the Micro, Small and Medium Enterprises Development Act, 2006.[2] The Act classifies them as micro, small and medium enterprises based on: (i) investment in plant and machinery for enterprises engaged in manufacturing or production of goods, and (ii) investment in equipment for enterprises providing services. As per the Cabinet approval, the investment limits will be revised upwards and annual turnover of the enterprise will be used as additional criteria for the classification of MSMEs (Table 1).

Earlier attempts to amend the definition of MSMEs

The central government has sought to revise the definition of MSMEs in the Act on two earlier occasions. The government introduced the MSME Development (Amendment) Bill, 2015 which proposed to increase the investment limits for manufacturing and services MSMEs.[3] This Bill was withdrawn in July 2018 and another Bill was introduced. The MSME Development (Amendment) Bill, 2018 proposed to: (i) use annual turnover as criteria instead of investment for classification of MSMEs, (ii) remove the distinction between manufacturing and services, and (iii) provide the central government with the power to revise the turnover limits, through a notification.[4] The 2018 Bill lapsed with the dissolution of 16th Lok Sabha.

Global trends in criteria for the classification of MSMEs

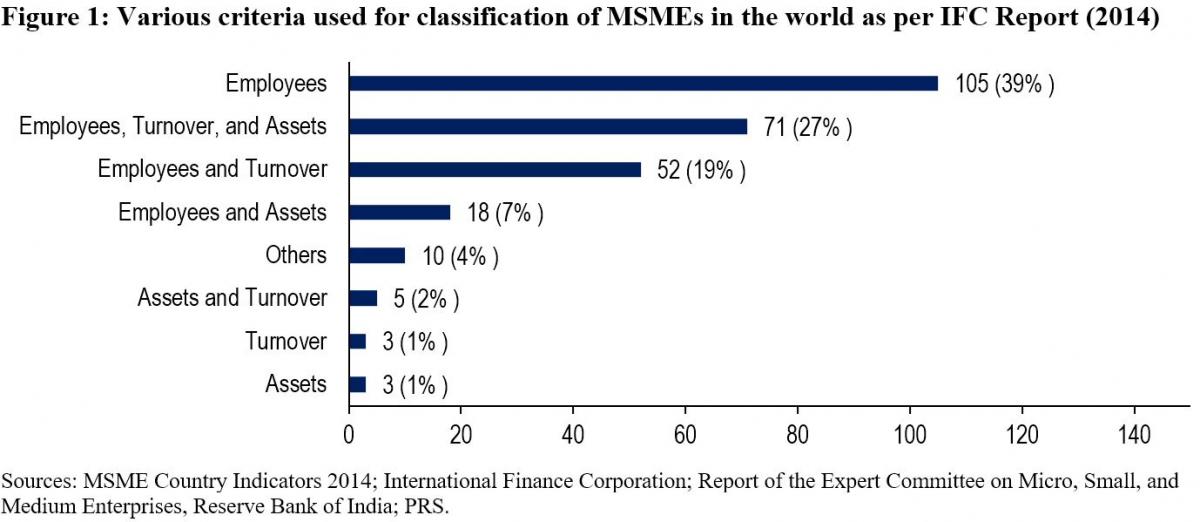

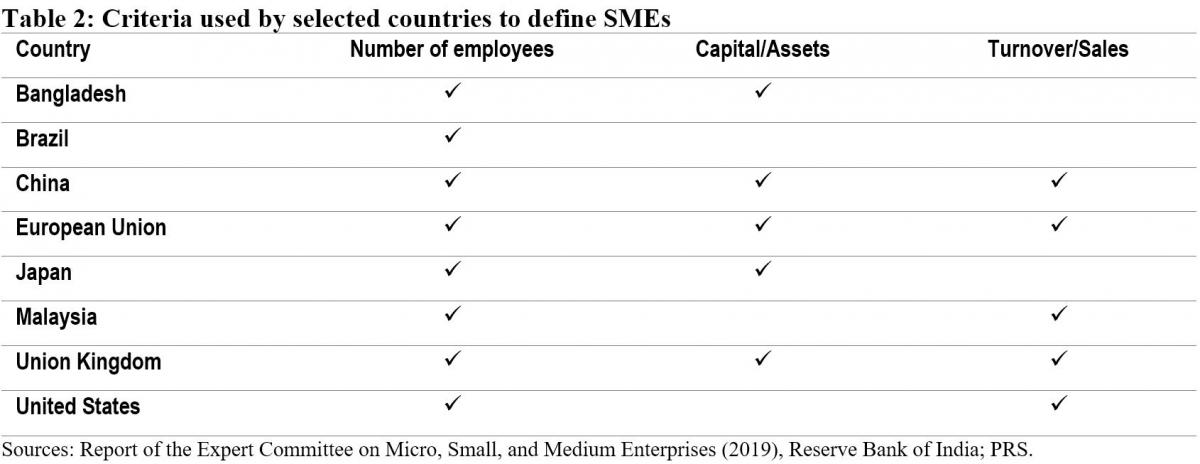

While India will now be using investment and annual turnover as the criteria to classify MSMEs, globally, the number of employees is the most widely used criteria for classifying MSMEs. The Reserve Bank of India's Expert Committee on MSMEs (2019) cited a study by the International Finance Corporation in 2014 which analysed 267 definitions used by different institutions in 155 countries.[5],[6] According to the study, countries used a combination of criteria to classify MSMEs. 92% of the definitions used the number of employees as one of the criteria. Other frequently used criteria were: (i) turnover (49%), and (ii) value of assets (36%). 11% of the analysed definitions used alternative criteria such as: (i) loan size, (ii) years of experience, and (iii) initial investment.

Evaluation of common criteria used to define MSMEs

Investment: The 2006 Act uses investment in plant, machinery, and equipment to classify MSMEs. Some of the issues with the investment criteria include:

Due to their informal and small scale of operations, firms often do not maintain proper books of accounts and hence find it difficult to get classified as MSMEs as per the current definition.5

The investment-based classification incentivises promoters to keep the investment size restricted to retain the benefits associated with the micro or small category.7

Turnover: The 2018 Bill sought to replace the investment criteria with annual turnover as the sole criteria for the classification of MSMEs. The Standing Committee agreed with the proposal under the Bill to use annual turnover as the criteria instead of investment.7 It observed that this could overcome some of the shortcomings of classification based on investment. While turnover based criteria will also require verification, the Committee noted that the GST Network (GSTN) data can act as a reliable source of information for this purpose. However, it also observed that:7

With turnover as a criterion for classification, corporates may misuse the incentives meant for MSMEs. For instance, there is a possibility that a multi-national company may produce a large quantity of products worth a high turnover and then market it through various subsidiaries registered as Micro or Small enterprise under GSTN.

The turnover of some enterprises may fluctuate depending on their business, which may result in the change of classification of the enterprise during a year.

The Committee noted that there is a wide gap in turnover limits. For instance, an enterprise with a turnover of Rs 6 crore and an enterprise with a turnover of Rs 75 crore (as proposed in 2018 Bill) would both be classified as a small enterprise, which seems incongruous.

The Expert Committee (RBI) also recommended using annual turnover as the criteria for classification instead of investment.5 It observed that turnover based definition would be transparent, progressive, and easier to implement through the GSTN. It also recommended that the power to change the definition of MSMEs should be delegated to the executive as it will help in responding to changing economic scenarios.

Number of employees: The Standing Committee had highlighted that in a labour-intensive country like India, appropriate focus is required on employment generation and MSME sector is the most suitable platform for this.7 It had recommended that the central government should assess the number of persons employed in the MSME sector and also consider employment as a criterion while classifying MSMEs. However, the Expert Committee (RBI) stated that while the employment-based definition is an additional feature preferred in some countries, the definition would pose challenges in implementation.5 According to the Ministry of MSME, employment as a criterion has problems due to: (i) factors such as seasonality and informal nature of engagement, (ii) similar to investment criteria, this would also require physical verification and has associated cost overheads.7

Number of MSMEs

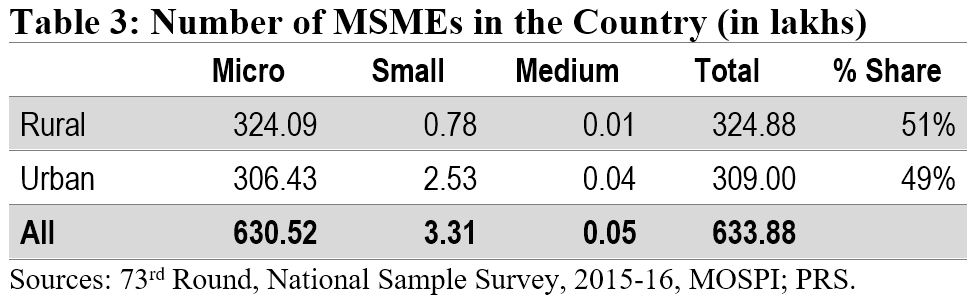

According to the National Sample Survey (2015-16), there were around 6.34 crore MSMEs in the country. The micro sector with 6.3 crore enterprises accounted for more than 99% of the total estimated number of MSMEs. The small and medium sectors accounted for only 0.52% and 0.01% of the estimated number of enterprises, respectively. Another dataset to understand the distribution of MSMEs is Udyog Aadhaar, a unique identity provided by the Unique Identification Authority of India (UIDAI) to MSME enterprises.[8] Udyog Aadhaar registration is based on self-declaration by enterprises. Between September 2015 and June 2020, 98.6 lakh enterprises have registered with UIDAI. According to this dataset, micro, small, and medium enterprises comprise 87.7%, 11.8% and 0.5% of the MSME sector respectively.

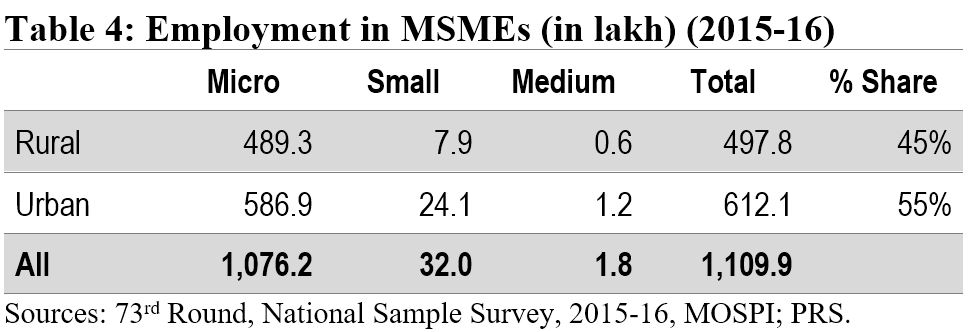

Employment in the MSME sector

The MSME sector employed nearly 11.1 crore people in 2015-16. The sector was the second largest employer after the agriculture sector. The highest number of employed persons were engaged in trade activity (35%), followed by persons engaged in manufacturing (32%).

Implications of change in the definition of MSMEs

The change in the definition of MSMEs may result in many enterprises which are currently classified as Small enterprises be reclassified as Micro, and those classified as Medium enterprises be reclassified as Small. Further, there may be many enterprises which are not currently classified as MSMEs, which may fall under the MSME classification as per the new definition. Such enterprises will also now benefit from the schemes related to MSMEs. The Ministry of MSME runs various schemes to provide for: (i) flow of credit to MSMEs, (ii) support for technology upgrade and modernisation, (iii) entrepreneurship and skill development, and (iv) cluster-wise measures to promote capacity-building and empowerment of MSME units. For instance, under the Credit Guarantee Fund Scheme for Micro and Small Enterprises, a credit guarantee cover of up to 75% of the credit is provided to micro and small enterprises.[9] Thus, the re-classification may require a significant increase in budgetary allocation for the MSME sector.

Other announcements related to MSMEs in the aftermath of COVID-19

MSME sector accounted for nearly 33.4% of the total manufacturing output in 2017-18.[10] During the same year, its share in the country’s total exports was around 49%. Between 2015 and 2017, the contribution of the sector in GDP has been around 30%. Due to the national lockdown induced by COVID-19, businesses including MSMEs have been badly hit. To provide immediate relief to the MSME sector, the government announced several measures in May 2020.[11] These include: (i) collateral-free loans for MSMEs with up to Rs 25 crore outstanding and up to Rs 100 crore turnover, (ii) Rs 20,000 crore as subordinate debt for stressed MSMEs, and (iii) Rs 50,000 crore of capital infusion into MSMEs. These measures have also been approved by the Union Cabinet.[12]

For more details on the announcements made under the Aatma Nirbhar Bharat Abhiyan, see here.

[1] “Cabinet approves Upward revision of MSME definition and modalities/ road map for implementing remaining two Packages for MSMEs (a)Rs 20000 crore package for Distressed MSMEs and (b) Rs 50,000 crore equity infusion through Fund of Funds”, Press Information Bureau, Cabinet Committee on Economic Affairs, June 1, 2020.

[2] The Micro, Small and Medium Enterprises Development Act, 2006, https://samadhaan.msme.gov.in/WriteReadData/DocumentFile/MSMED2006act.pdf.

[3] The Micro, Small and Medium Enterprises Development (Amendment) Bill, 2015, https://www.prsindia.org/sites/default/files/bill_files/MSME_bill%2C_2015_0.pdf.

[4] The Micro, Small and Medium Enterprises Development (Amendment) Bill, 2018, https://www.prsindia.org/sites/default/files/bill_files/The%20Micro%2C%20Small%20and%20Medium%20Enterprises%20Development%20%28Amendment%29%20Bill%2C%202018%20Bill%20Text.pdf.

[5] Report of the Expert Committee on Micro, Small and Medium Enterprises, The Reserve Bank of India, July 2019, https://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/MSMES24062019465CF8CB30594AC29A7A010E8A2A034C.PDF.

[6] MSME Country Indicators 2014, International Finance Corporation, December 2014, https://www.smefinanceforum.org/sites/default/files/analysis%20note.pdf.

[7] 294th Report on Micro Small and Medium Enterprises Development (Amendment) Bill 2018, Standing Committee on Industry, Rajya Sabha, December 2018, https://rajyasabha.nic.in/rsnew/Committee_site/Committee_File/ReportFile/17/111/294_2019_3_15.pdf.

[8] Enterprises with Udyog Aadhaar Number, National Portal for Registration of Micro, Small & Medium Enterprises, Ministry of Micro, Small and Medium Enterprises, https://udyogaadhaar.gov.in/UA/Reports/StateBasedReport_R3.aspx.

[9] Credit Guarantee Fund Scheme for Micro and Small Enterprises, Ministry of Micro, Small and Medium Enterprises, http://www.dcmsme.gov.in/schemes/sccrguarn.htm.

[10] Annual Report 2018-19, Ministry of Micro, Small and Medium Enterprises, https://msme.gov.in/sites/default/files/Annualrprt.pdf.

[11] "Finance Minister announce measures for relief and credit support related to businesses, especially MSMEs to support Indian Economy’s fight against COVID-19", Press Information Bureau, Ministry of Finance, May 13, 2020.

[12] "Cabinet approves additional funding of up to Rupees three lakh crore through introduction of Emergency Credit Line Guarantee Scheme (ECLGS)", Press Information Bureau, Ministry of Finance, May 20, 2020.